The Market Nobody's Talking About: Why Anti-Submarine Warfare AI Is Quietly Booming

While most defense-tech headlines this year have gone to drones, hypersonics, and space-based systems, a quieter but structurally larger shift has been building underwater. Anti-submarine warfare (ASW) — historically one of the slowest-moving, most conservative corners of naval procurement — is in the middle of a genuine boom, and artificial intelligence is the layer making it possible. The market numbers vary a lot depending on which research firm you ask, but every single estimate points the same direction: up, and accelerating. This piece breaks down the market sizing, the segment-level detail behind it, the regional race, who's actually building the technology, and what it means for teams working in Defence AI.

The Numbers, and Why They Don't Agree

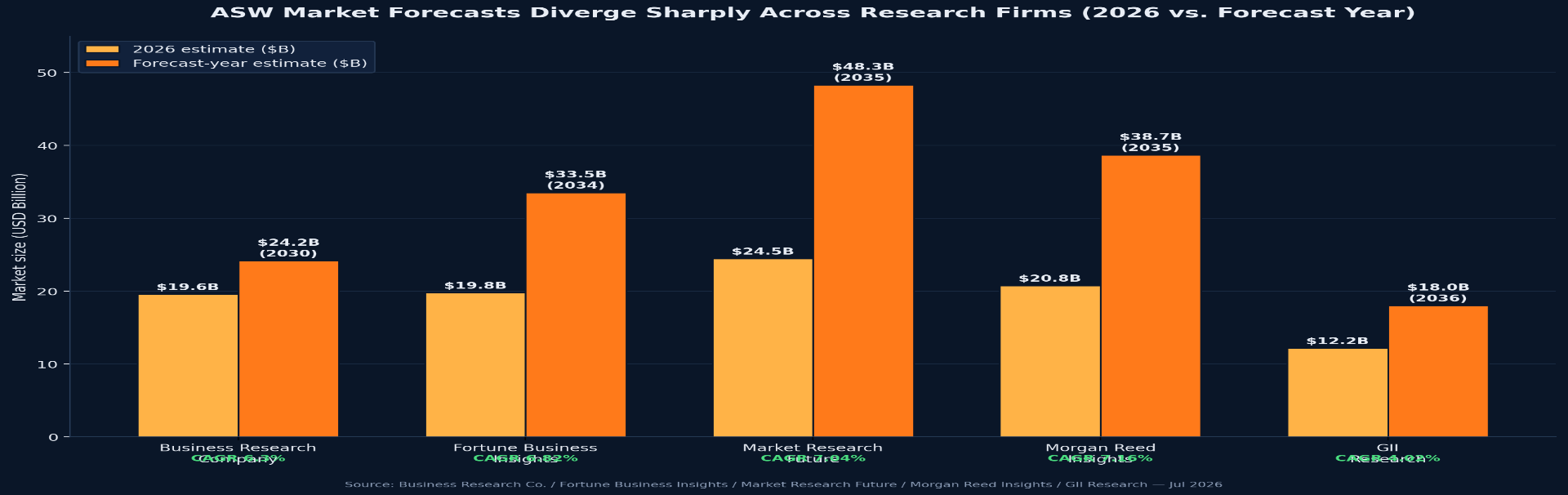

Ask five different market research firms what the ASW market is worth in 2026, and you'll get five different answers — not because anyone is wrong, but because "anti-submarine warfare market" gets scoped differently depending on whether a firm counts full platforms (frigates, submarines, aircraft) or narrows to sensors and systems alone. The Business Research Company puts the global ASW systems market at $19.59 billion in 2026, growing at a 6.3% CAGR toward $24.2 billion by 2030. Fortune Business Insights pegs 2026 at a very similar $19.77 billion but projects a much steeper climb to $33.52 billion by 2034. Market Research Future is the most bullish of the group, estimating $24.47 billion in 2025 growing to $48.33 billion by 2035 at a 7.04% CAGR — nearly a doubling. Morgan Reed Insights, focused specifically on the AI-and-autonomy angle, sizes the market at $20.76 billion in 2026 rising to $38.69 billion by 2035, while GII Research's more conservative scope puts 2026 at just $12.16 billion, growing modestly to $18.03 billion by 2036.

What's consistent across every single one of these divergent estimates is the direction and the drivers: every firm cites naval modernization, rising geopolitical tension, and — increasingly — the shift toward AI-enabled, autonomous, and networked detection systems as the core growth engine, not just bigger defense budgets buying more of the same old sonar buoys. It's also worth noting that a closely related category, the broader "undersea warfare systems" market — which folds in mine warfare alongside ASW — is separately estimated at $22.6 billion in 2026, growing at 6.9% CAGR to $28.51 billion by 2030, reinforcing that whichever way you slice the definition, the underlying trend line is the same.

Table 1 — Market Size Estimates by Research Firm

Research Firm

2026 Estimate

Forecast Year

Forecast Value

CAGR

The Business Research Company

$19.59B

2030

$24.2B

6.3%

Fortune Business Insights

$19.77B

2034

$33.52B

6.82%

Market Research Future

$24.47B (2025)

2035

$48.33B

7.04%

Morgan Reed Insights

$20.76B

2035

$38.69B

7.16%

GII Research

$12.16B

2036

$18.03B

4.02%

The Business Research Co. (Undersea Warfare, broader scope)

$22.6B

2030

$28.51B

6.0–6.9%

Strategic Market Research

$18.6B (2024)

2030

$26.1B

5.8%

What's Actually Driving the Growth

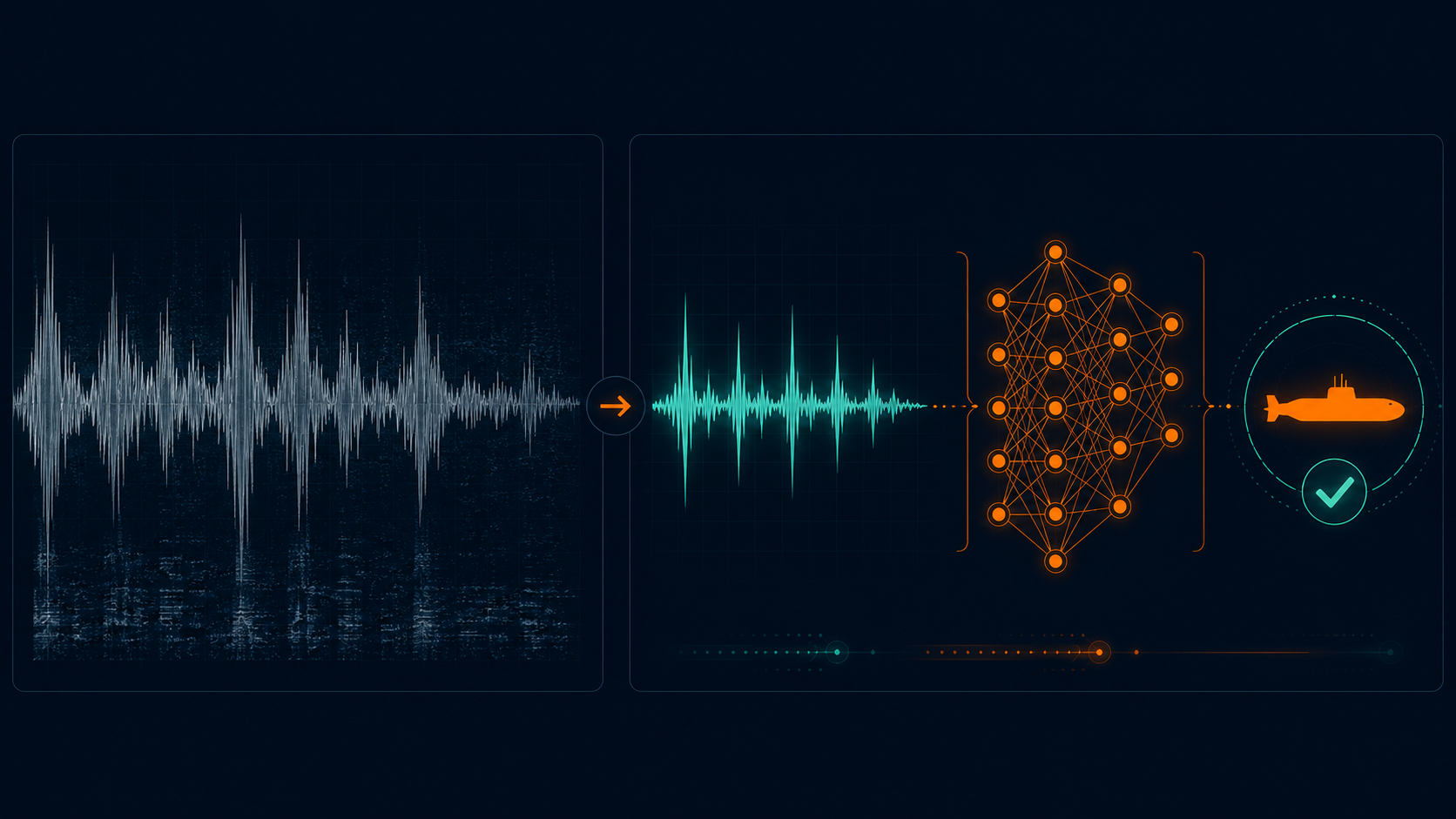

Three forces stand out. First, submarine proliferation: near-peer navies — particularly China's — have expanded both the number and the acoustic sophistication of their submarine fleets, eroding the acoustic-signature advantage NATO navies relied on for decades. Second, defense-spending momentum: global defense expenditure hit a record $2.46 trillion in 2024, up 7.4% year-on-year, giving navies more room to fund modernization rather than just sustainment. Third, and most relevant to this newsletter, is the technology shift itself — a move from procuring more of the same platform-centric sonar buoys toward integrated, AI-enabled detection ecosystems that fuse acoustic, magnetic, and even non-acoustic sensor data into a single classification pipeline.

Fortune Business Insights frames the entire technology stack this way: sonar systems in both passive and active modes, towed detection arrays, lightweight torpedoes, and — critically — "acoustic processing with artificial intelligence systems," alongside more advanced command-and-control layers that coordinate a faster response once a contact is classified. That last piece, AI-driven acoustic signal processing, is repeatedly singled out across multiple reports as the single most transformative element reshaping the sector, more so than any new hull or weapon type.

Market Segmentation: Where the Money Actually Goes

Beyond the headline numbers, most research firms break the ASW market down along three consistent axes: system type, platform, and end user. On system type, the market splits roughly across sonar systems (both passive and active), electronic support measures, and armament — torpedoes, depth charges, and missile systems — with sonar and acoustic processing consistently identified as the fastest-growing sub-segment because it's where AI integration is happening first and fastest. On platform, the market covers submarines, surface ships (frigates, destroyers, corvettes), helicopters, maritime patrol aircraft, and unmanned systems — and unmanned underwater and surface vehicles are flagged across nearly every report as the fastest-growing platform category, even though traditional surface ships still hold the largest absolute share of spending today. On end user, naval forces are overwhelmingly the dominant buyer, with aerospace and defense contractors making up the remainder as system integrators and suppliers rather than direct operators.

Table 2 — Market Segmentation Snapshot

Segment Axis

Categories

Fastest-Growing Sub-Segment

Why

System Type

Sonar, Electronic Support Measures, Armament

Sonar / acoustic processing

First and fastest area for AI integration

Platform

Submarines, Surface Ships, Helicopters, MPA, Unmanned Systems

Naval Forces (dominant, not fastest-growing but largest)

Direct procurement authority

Detection Mode

Active Sonar, Passive Sonar, Magnetic Anomaly Detection, AI-Enabled Acoustic Processing

AI-enabled acoustic processing

Enables multi-sensor fusion at scale

Regional Picture: North America Leads, Asia-Pacific Sprints

North America held the largest regional share of the ASW market in 2025, at roughly $6.53 billion, growing to about $7.04 billion in 2026 — a position built on the sheer scale of U.S. naval procurement, deep investment in advanced sensing technology, and long-running submarine modernization programs. The U.S. alone accounted for around $6.05 billion of that in 2025.

Europe is the fastest-growing established market, projected at a 7.34% CAGR off a 2025 base of roughly $4.05 billion — a trajectory directly linked to NATO's collective push toward significantly higher defense spending commitments, much of it flowing into exactly the kind of undersea-infrastructure protection discussed in our companion piece on the Baltic Sea cable sabotage. NATO's broader spending trajectory reinforces this: the UK alone has committed to raising defense spending to 2.6% of GDP from 2027, with a meaningful share earmarked for the undersea and autonomy programs discussed in our companion DASH/TRAPS/SHARK piece.

But the real long-term growth story is Asia-Pacific, repeatedly flagged across multiple reports as the fastest-growing region overall, driven by naval modernization in China, India, Japan, and South Korea, and by intensifying regional maritime disputes. Japan's ASW market alone was valued at $0.82 billion in 2025, growing at a 6.88% CAGR — a small base, but one of the steepest growth rates in the entire sector. Australia's position is especially notable given the AUKUS submarine partnership: beyond acquiring nuclear-powered Virginia-class and future SSN-AUKUS submarines, Australia is co-developing shared uncrewed underwater vehicle payloads with the US and UK under a signature Pillar 2 project announced in May 2026, with first capabilities expected in service by 2027 — a direct pipeline from R&D spending into fielded ASW-AI capability.

The competitive landscape is dominated by the traditional prime contractors you'd expect — Lockheed Martin, Raytheon Technologies (RTX), Northrop Grumman, BAE Systems, Thales Group, General Dynamics, Leonardo, and L3Harris — alongside specialized undersea-systems players like Leidos, Elbit Systems, Kongsberg, DSIT Solutions, Mitsubishi Heavy Industries, Huntington Ingalls Industries, Fincantieri, Kawasaki Heavy Industries, Aselsan, Navantia, and Garden Reach Shipbuilders & Engineers. Naval forces remain the dominant end-user segment by a wide margin, and unmanned underwater vehicles are consistently flagged as the fastest-growing platform sub-segment — a direct continuation of the distributed, autonomous-sensing philosophy that programs like DARPA's DASH (covered in our companion piece) pioneered over a decade ago.

Newer entrants are also reshaping the competitive picture, particularly in the uncrewed-systems segment. Companies like Anduril, whose Ghost Shark extra-large autonomous underwater vehicle has moved from prototype into AUKUS-linked development pipelines, represent a broader trend of venture-backed defense-tech firms competing directly with legacy primes for autonomy and AI-software contracts — a segment where software and machine-learning expertise increasingly matters as much as traditional shipbuilding or sonar-hardware experience.

Huntington Ingalls Industries, Fincantieri, Navantia, Mitsubishi Heavy Industries, Kawasaki Heavy Industries, Garden Reach Shipbuilders & Engineers

Regional / Emerging Defense Firms

Aselsan (Turkey)

Autonomy / Software-First Entrants

Anduril (Ghost Shark UUV), various AUKUS Innovation Challenge winners

Market Restraints Worth Noting

It's not all one-directional growth. Every major report flags similar headwinds: the extremely long procurement and testing cycles typical of naval hardware, which can stretch a decade from prototype to fleet integration (as the DASH story illustrates); high per-unit costs for advanced sonar and UUV platforms that limit how many smaller navies can realistically field them; and a persistent shortage of specialized undersea engineering talent, which constrains how fast even well-funded programs can scale. There's also a structural tension in the market between exquisite, expensive platforms and DASH-style distributed, "good enough" sensor networks — a tension every navy is currently negotiating differently based on its budget and threat environment.

What This Means Going Forward

Put together, the Baltic Sea cable incidents, the DASH-to-TRAPS/SHARK pipeline, and this market data tell a single coherent story: undersea infrastructure and submarine detection have moved from a Cold War legacy concern to an active, well-funded priority again, and the growth is concentrated specifically in the AI and autonomy layer rather than in traditional hardware. For teams working in Defence AI, that translates into real opportunity across acoustic signal classification, multi-sensor data fusion, anomaly detection for maritime domain awareness, and autonomous UUV navigation and control — areas where research novelty and defense relevance currently overlap more than almost anywhere else in the sector, and where the market data suggests the funding will keep flowing for at least the next decade regardless of which forecast turns out closest to reality.

Sources

Fortune Business Insights — Anti-Submarine Warfare Market Report

The Business Research Company — Anti-Submarine Warfare Systems & Undersea Warfare Systems Global Market Reports 2026

Market Research Future — Anti-Submarine Warfare Market Report

Morgan Reed Insights — Anti-Submarine Warfare Market Analysis

GII Research — Global Anti-Submarine Warfare Market 2026–2036

Strategic Market Research — Anti-Submarine Warfare Market 2026 Report

International Institute for Strategic Studies (IISS) — Global Defense Expenditure Data, February 2025

GOV.UK / UK Ministry of Defence — AUKUS Pillar 2 announcements, May 2026

Breaking Defense — AUKUS underwater drone agreement coverage, June 2026