GE Aerospace: The OEM Giant Betting Its MRO Network on AI Shop-Visit Prediction

Company Report: GE Aerospace — The OEM Giant Betting Its MRO Network on AI Shop-Visit Prediction

1. Company Snapshot

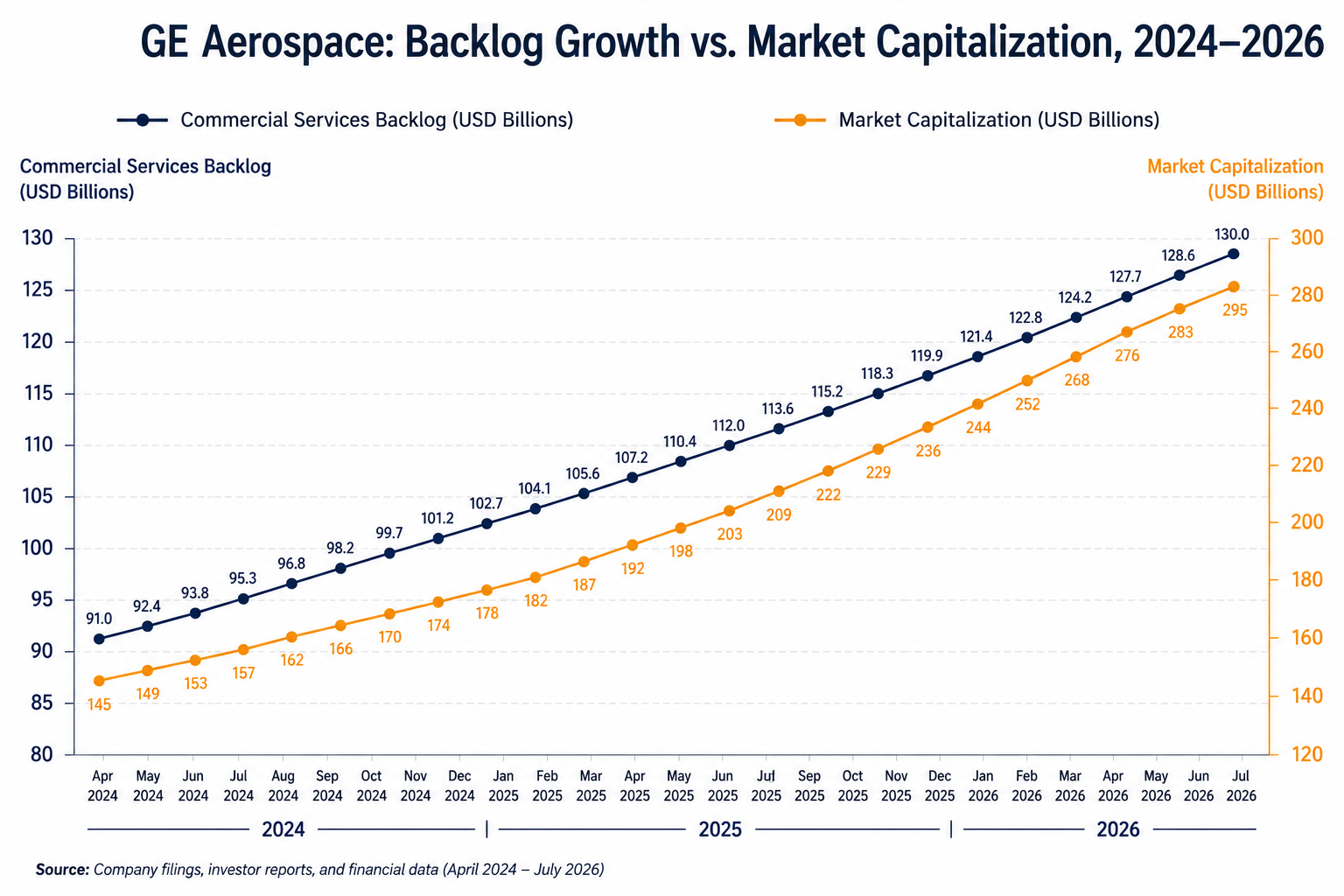

GE Aerospace is the world's largest jet engine manufacturer and MRO (maintenance, repair, and overhaul) services provider by installed base, formally re-established as a standalone public company in April 2024 following the multi-year breakup of the historic General Electric conglomerate (which also spun off GE Vernova and, earlier, GE HealthCare). Its business splits into two reporting segments — Commercial Engines & Services and Defense & Propulsion Technologies — and its defining commercial asset is CFM International, its 50/50 joint venture with Safran Aircraft Engines, which produces the LEAP engine family powering the Boeing 737 MAX exclusively and roughly three-quarters of new Airbus A320neo orders. The company's central strategic bet, and the subject of this report, is that AI-driven predictive maintenance — digital twins built at the individual engine level, work-scope forecasting, and computer-vision inspection — can be deployed across this installed base to reshape the economics of a services backlog that has grown past $170B.

| Attribute | Detail |

|---|---|

| Founded | Aviation lineage traces to 1917 (GE's original aviation engineering work); re-established as an independent, standalone public company via corporate spin-off on April 2, 2024 |

| HQ | Evendale, Ohio (Greater Cincinnati area), United States |

| Founders/CEO | Parent company (General Electric) founded 1892, associated with Thomas Edison; current Chairman & CEO of GE Aerospace: H. Lawrence "Larry" Culp Jr. |

| Total Funding | Not applicable in the venture sense — GE Aerospace is a publicly traded spin-off (NYSE: GE) with no disclosed private/VC funding rounds; capital structure is public equity plus corporate debt |

| Latest Valuation (Market Cap) | Approximately $385–390B as of late June/early July 2026 <br>[VERIFY: exact figure on date of publication, as this moves daily with the share price] |

| Employee count | Approximately 57,000 globally (as of mid-2026) |

2. What They Actually Build

Strip away the corporate branding and GE Aerospace's core offering is jet engines plus the multi-decade maintenance relationship attached to every one of them — with AI increasingly embedded in that second half of the business rather than the first.

Engine hardware. GE Aerospace designs and manufactures commercial turbofans (the GE9X for the Boeing 777X, the GEnx for the 787 and 747-8, and the LEAP family via CFM International) and military engines (the F110, F404, T700, and T901, among others) covering the large majority of U.S. military combat and helicopter fleets. It also produces components under the Avio Aero, Unison, Dowty Propellers, and Colibrium Additive brands.

The services relationship. The commercially and financially dominant part of the business is not selling engines — it's maintaining them for 20-30 years afterward under long-term service agreements (LTSAs), time-and-material shop visits, and spare parts sales, which together carry operating margins above 20%, roughly double the margin on new equipment.

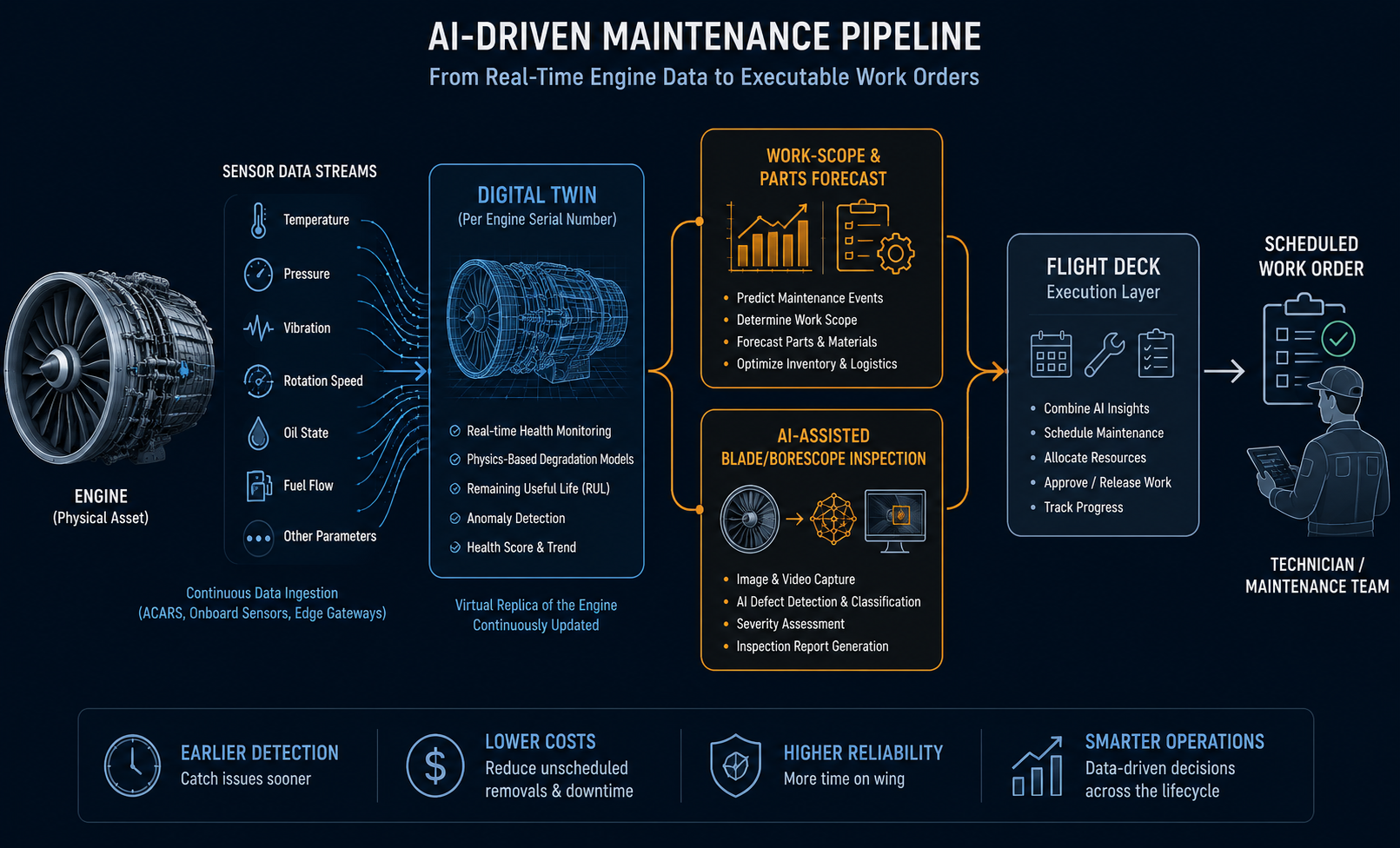

The AI layer sitting on top of that relationship. GE Aerospace builds engine-serial-number-specific digital twins from on-wing sensor data (vibration, temperature, fuel flow) to forecast component wear individually rather than off fleet averages; uses that forecasting to predict a specific engine's shop-visit work scope and parts needs months before it's actually inducted for maintenance; deploys AI-assisted computer-vision inspection (developed for the GEnx, GE9X, and LEAP families, and via a partnership with Waygate Technologies for borescope inspection) to assess blade erosion and coating integrity; and is developing a GenAI maintenance-records assistant with Accenture and Microsoft to automate compliance documentation. All of this sits inside FLIGHT DECK, GE Aerospace's proprietary lean operating model, which the company describes as the discipline that converts a predictive insight into an actual part arriving at the right shop on the right day — a distinction the company treats as at least as important as the predictive model itself.

3. Recent Moves (Last ~6–12 Months)

GE Aerospace's last year of public disclosures shows a company simultaneously posting strong financial results, expanding its AI/board-level tech credibility, and managing real execution strain from demand outpacing its supply chain.

Q1 2026 earnings (reported April 2026). Orders surged roughly 87% year-over-year, driven heavily by Commercial Engine Services; revenue reached $11.6B against a $10.71B estimate; adjusted EPS of $1.86 beat the $1.60 consensus; and free cash flow rose 14% to $1.7B — though the stock still fell on the day, reflecting investor sensitivity to a roughly 200-basis-point operating margin decline the company attributed to strategic investment spend and inflation, even as operating profit itself grew 18% on 29% revenue growth. Full-year 2026 EPS guidance stands at $7.47, with FY2027 guided to $8.44.

Microsoft AI leadership added to the board (June 10, 2026). GE Aerospace added a Microsoft AI executive to its board of directors — a direct signal, alongside the Accenture/Microsoft GenAI Assistant collaboration, that the company is treating AI/software leadership as a board-level governance priority, not just an engineering initiative.

Wolfspeed MOU on silicon carbide (SiC) semiconductors (June 7, 2026). GE Aerospace signed a memorandum of understanding with Wolfspeed to accelerate adoption of SiC power semiconductors — relevant to more-electric and hybrid-electric propulsion systems and power-dense onboard electronics, an adjacent but distinct bet from the predictive-maintenance AI story, worth watching as a signal of where GE Aerospace sees its next technology curve.

China engine order discussions (reported early June 2026). GE Aerospace has signaled it believes it can secure additional engine orders from China, per Bloomberg reporting — a geopolitically sensitive area given ongoing U.S. export-control dynamics around aerospace technology sales to China.

LEAP-1B durability kit certification (expected H1 2026). GE Aerospace has targeted first-half-2026 certification of a durability improvement kit for the LEAP-1B engine (exclusive powerplant on the Boeing 737 MAX), addressing a known pattern of earlier-than-projected shop visits — though full fleet-wide benefit will take years to propagate as engines cycle through scheduled maintenance.

4. Competitive Position

GE Aerospace is frequently described as holding the strongest moat in industrial aerospace: proprietary engine IP, a 25-30-year service tail per engine sold, FAA-approved maintenance data exclusivity, and the CFM International joint venture with Safran. Its most direct like-for-like propulsion competitor is RTX Corporation's Pratt & Whitney division, with Rolls-Royce as the closest widebody-specific competitor.

| Dimension | GE Aerospace | Pratt & Whitney (RTX) |

|---|---|---|

| Core narrowbody position | LEAP (via CFM International) holds roughly 70-76% share on the Airbus A320neo family and is the exclusive engine on the Boeing 737 MAX | GTF holds the remaining ~24-30% A320neo share; no 737 MAX presence |

| Recent reliability track record | LEAP-1B durability kit in progress to address earlier-than-projected shop visits; broadly favorable reliability narrative versus GTF | GTF program has been affected by widely reported powder-metal contamination issues requiring accelerated inspections and removals |

| Installed base / data scale | More than 44,000 commercial engines and roughly 30,000+ military engines in service — the industry's largest dataset for training predictive models | Smaller installed base; investing in comparable digital twin and predictive maintenance capability but starting from a smaller data pool |

| Services backlog scale | Commercial services backlog exceeding $170B; total company backlog over $210B (Q1 2026) | [VERIFY: RTX/Pratt & Whitney segment-specific services backlog figure] |

| Stated AI/digital differentiation | Named, specific capabilities: engine-serial-number digital twins, advance work-scope/parts forecasting, computer-vision inspection, GenAI maintenance-records assistant, Microsoft AI board representation | Investing in similar digital twin and predictive maintenance capability; less publicly granular disclosure of specific named AI tools as of this writing |

Rolls-Royce, for context, competes credibly on widebody engines (notably the Trent XWB) but has no meaningful narrowbody position after losing the LEAP competition decades ago, and has itself undergone a significant turnaround in 2025 under continued investment in similar predictive maintenance and digital twin technology. Beyond direct engine OEMs, Airbus's Skywise platform (used by more than 130 airlines) and Boeing's AnalytX tools represent a different competitive vector worth tracking: airframers and airlines building parallel data science capability that could, over time, take on some diagnostic work currently performed inside OEM service centers like GE Aerospace's.

5. Why It Matters

GE Aerospace's predictive maintenance program is arguably the clearest large-scale, revenue-linked proof point currently available that AI-driven maintenance forecasting changes contract economics, not just operational efficiency: a services backlog exceeding $170B, priced years in advance under LTSAs built on averaged wear assumptions, is being actively renegotiated in effect — engine by engine — by digital twins that extend or shorten time-on-wing based on individual sensor data. For the broader defense-AI industry, this matters as a signal that predictive maintenance AI has moved well past the pilot-program stage into production deployment tied directly to a public company's quarterly earnings calls and investor guidance — a materially higher bar of accountability than most published defense-AI case studies operate under. It also illustrates a structural pattern worth generalizing: the OEM with the largest installed base (and therefore the largest training dataset) has a real, if not unlimited, data advantage — but that advantage only converts to margin if the surrounding operational discipline (GE Aerospace's FLIGHT DECK model) can actually act on what the models predict, a distinction with direct relevance to any organization evaluating AI-driven maintenance claims from a vendor or OEM.

6. Chart Data Table

(Note: GE Aerospace is a publicly traded corporate spin-off, not a venture-funded company — there are no priced equity funding rounds in the traditional startup sense. The table below is adapted to track the two financial metrics most relevant to this report's thesis: services backlog growth and public market capitalization, both directly tied to the AI-driven predictive maintenance narrative.)

Funding Timeline Data (Adapted: Market Cap & Backlog Timeline)

| Milestone | Date | Commercial Services Backlog ($B) | Market Capitalization ($B) |

|---|---|---|---|

| Spin-off from General Electric (independent public company) | April 2, 2024 | [VERIFY: backlog at spin-off] | [VERIFY: market cap at spin-off] |

| Year-end 2025 (Q4 2025 earnings) | ~Dec 2025 | ~$170B (total backlog ~$190B) | [VERIFY] |

| Q1 2026 earnings | April 2026 | >$170B (total backlog >$210B) | [VERIFY: market cap at report date] |

| All-time high share price | July 2, 2026 | N/A | ~$383–385B (implied, at $382.97/share) |

| Latest available market cap | June 26 – July 1, 2026 | N/A | $385–390B [VERIFY: exact figure on publication date] |