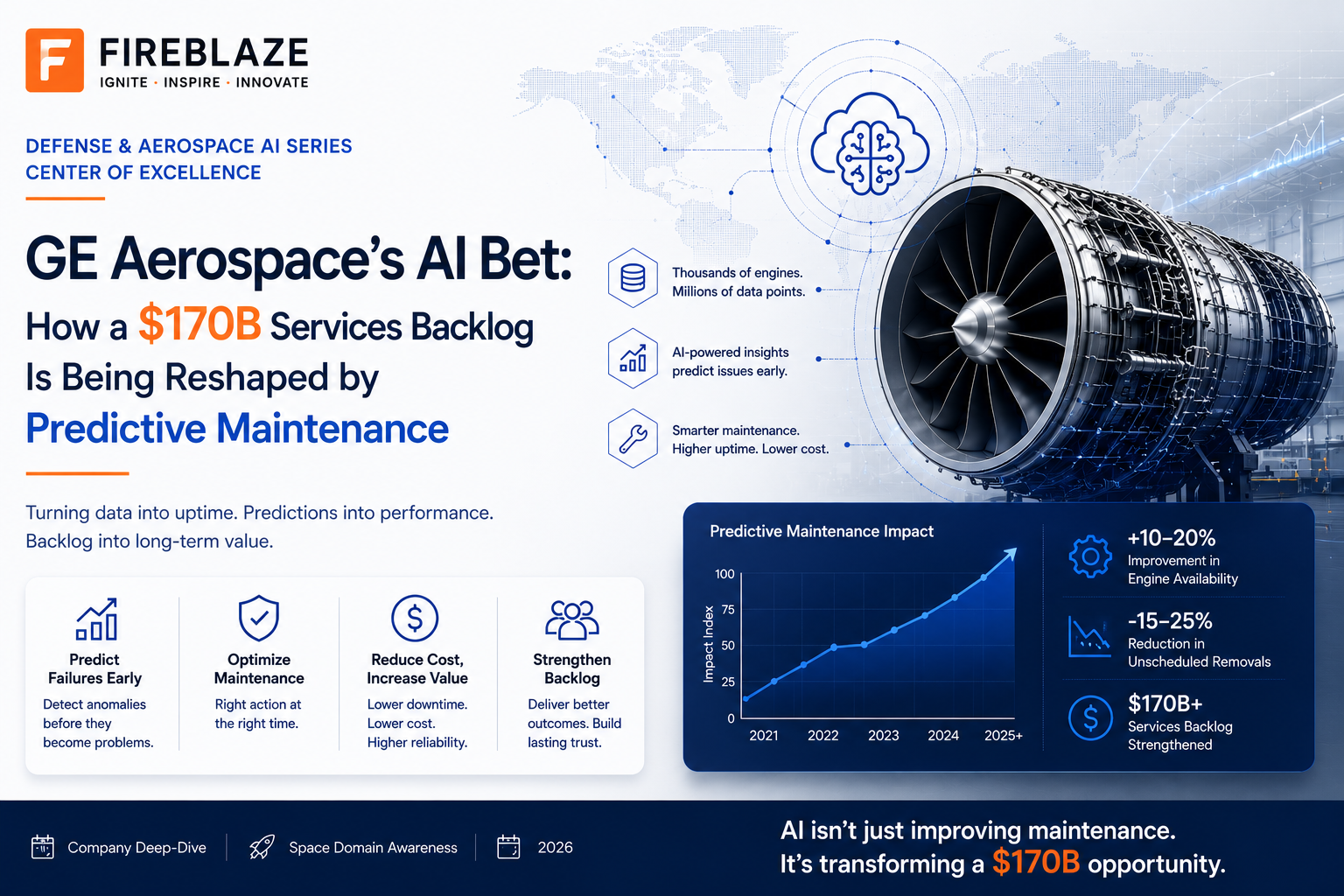

GE Aerospace's AI Bet: How a $170B Services Backlog Is Being Reshaped by Predictive Maintenance

GE Aerospace's AI Bet: How a $170B Services Backlog Is Being Reshaped by Predictive Maintenance

The largest jet engine services franchise in the world is betting that AI doesn't threaten its aftermarket moat — it deepens it.

1. What Happened

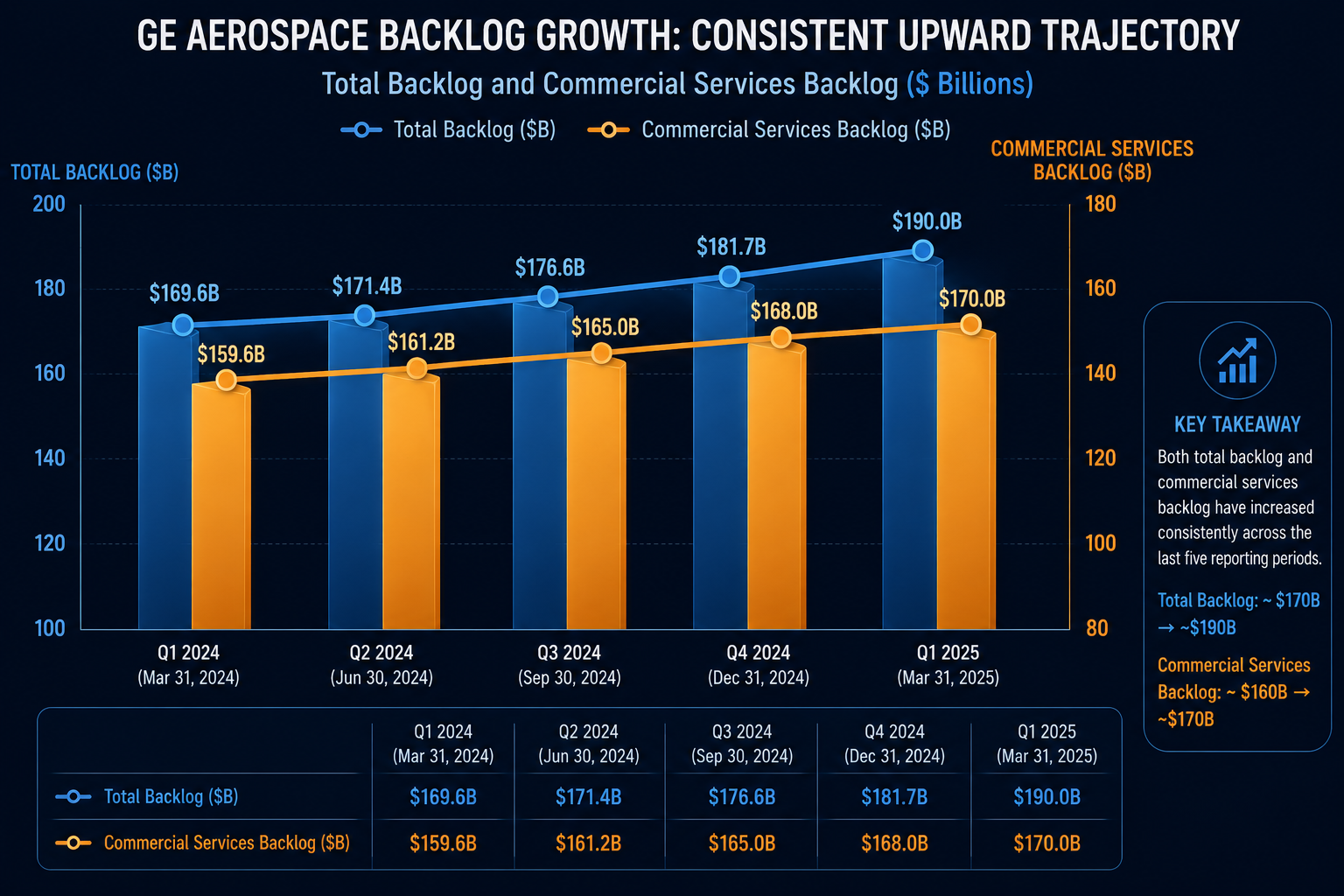

GE Aerospace closed 2025 with a total backlog of approximately $190 billion (roughly $170 billion of it commercial services), up nearly $20 billion year-over-year, and followed with a strong first-quarter 2026 in which orders grew 87% and services revenue climbed 39%. In parallel, the company has been rapidly deepening an AI partnership with Palantir Technologies — expanded again in March 2026 — that now orchestrates predictive maintenance, supply-chain allocation, and repair scheduling across both its military and commercial engine fleets, alongside its internally branded "FLIGHT DECK" lean operating system.

(Note: the $160B figure referenced in some industry commentary reflects GE's commercial services backlog as of late 2025/early 2026; the company's own Q1 2026 disclosure puts commercial services backlog at $170 billion and total backlog at roughly $190 billion — the underlying trend is growth, not the specific figure staying fixed. See the backlog timeline table in Section 3.)

2. Why It Matters

GE Aerospace is a useful lens for understanding where AI actually creates value in industrial aftermarket services, because the company sits on possibly the most AI-resistant revenue base in aerospace — and is choosing to lean into AI anyway, which tells you something important about where the real opportunity is.

2.1 The Backlog Is Structurally Insulated From AI Disruption — Which Is Exactly Why GE Is Investing in AI at the Margin

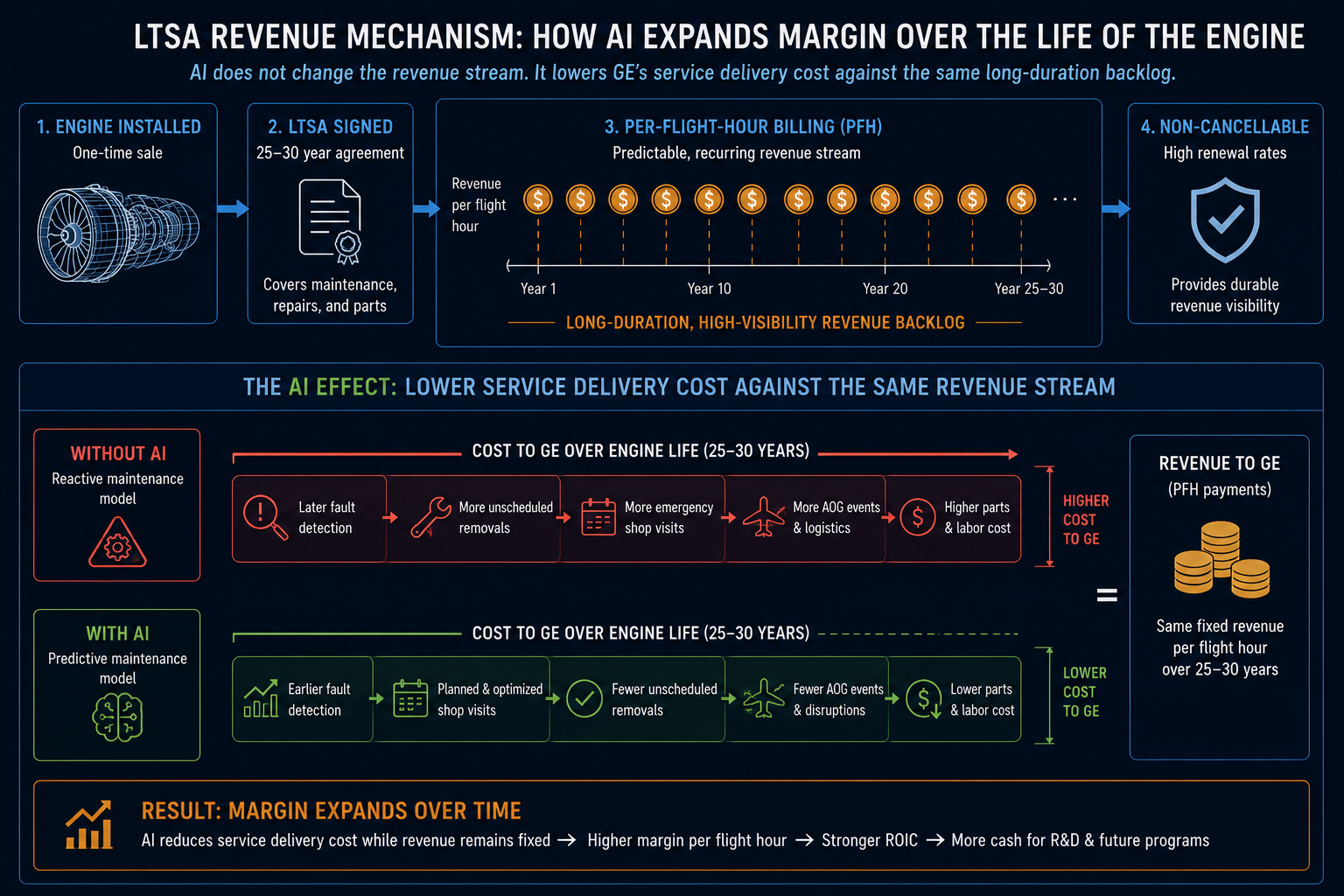

Airlines cannot switch engine manufacturers mid-life; once a LEAP or CFM56 engine is installed, it generates a service revenue stream for roughly 25–30 years under long-term service agreements (LTSAs) that typically bill per flight hour regardless of when the actual shop visit occurs. With more than 10,000 LEAP engines still in backlog and most not reaching their first major shop visit until the late 2020s, GE's aftermarket revenue wave is effectively pre-committed for years. This matters because it reframes what AI is actually being deployed to do here: it isn't defending market share against disruption, it's compressing cost and improving margin on services that were already contractually secured — a meaningfully different, lower-risk value proposition than most "AI will disrupt this industry" narratives assume. The economics only work in GE's favor if service delivery gets cheaper and faster per engine, which is precisely the lever predictive maintenance is designed to pull.

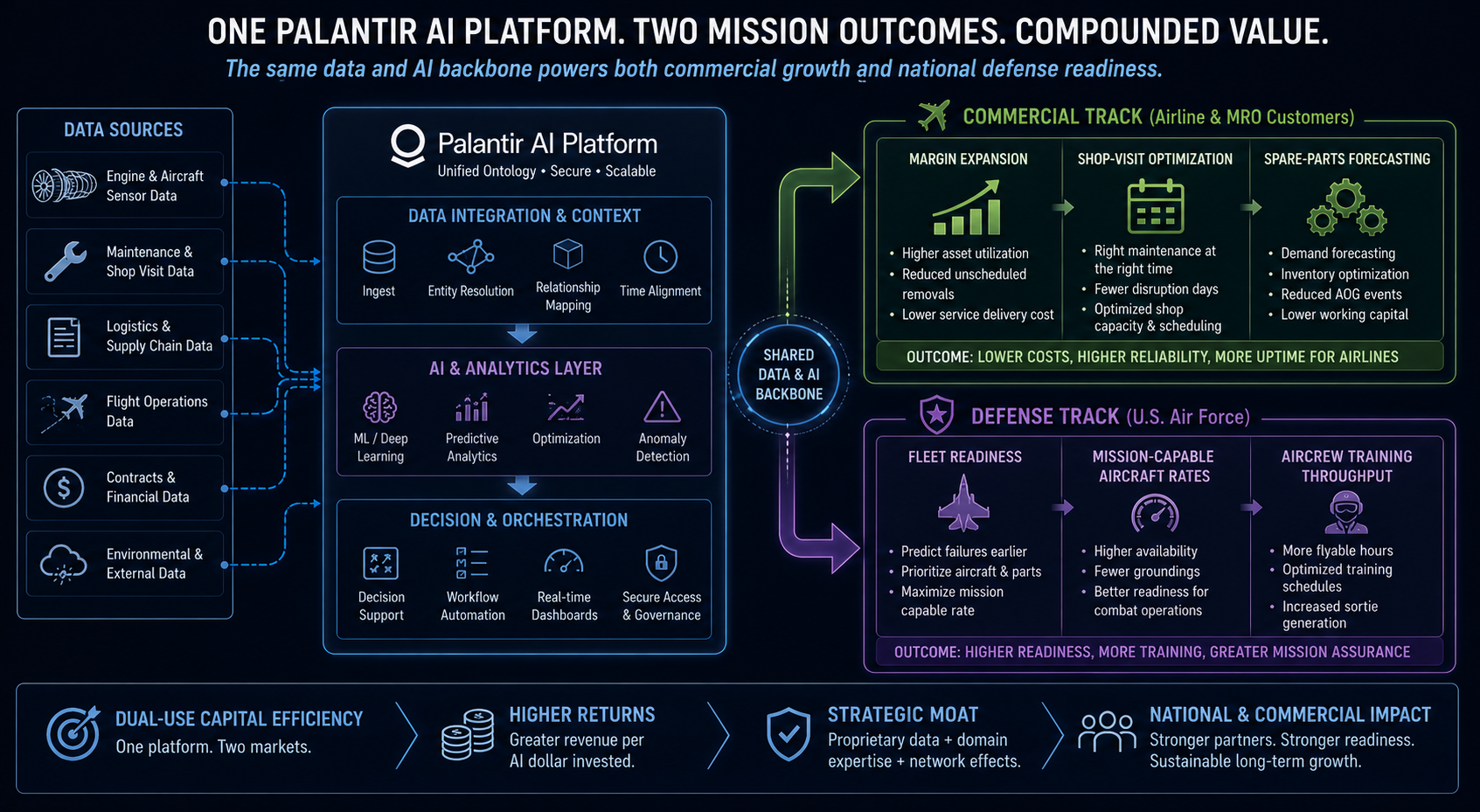

2.2 The Palantir Partnership Is the Clearest Evidence of Where GE Sees the Real Money

What started as a narrower effort to improve sustainment of the U.S. Air Force's T-38 trainer jet engines has expanded into a broader architecture — described in GE's own materials as a "TrueChoice Defense" ecosystem — that unifies data across fulfillment, sourcing, allocation, maintenance, repair, and customer service, giving GE and the Air Force real-time visibility into engine health worldwide and predictive alerts on parts failures before they occur. Separate industry reporting on GE's broader predictive-maintenance rollout (developed with Palantir Foundry) cites detecting engine issues roughly 60% earlier and cutting unscheduled engine removals by around 33% — figures that, if they hold up at fleet scale, translate directly into fewer AOG (Aircraft on Ground) events, better spare-parts forecasting, and reduced excess inventory, which is precisely the cost structure a $170 billion backlog needs to service efficiently as delivery volumes ramp.

2.3 This Is a Two-Sided Bet: Commercial Margin Expansion and Defense Readiness, Running on the Same Stack

On the commercial side, independent analysis has estimated predictive maintenance, digital twin simulation, and AI-optimized shop-visit scheduling could represent a $500 million to $1 billion annual margin opportunity for GE by 2028 — not by winning new engine placements, but by extracting more efficient service delivery from engines already locked into GE's aftermarket network. On the defense side, the Palantir expansion is explicitly framed around fleet "readiness" — keeping more aircraft mission-capable and more aircrew trained — a metric the Department of Defense cares about independent of GE's own margins, which gives GE a second, non-commercial buyer for the same underlying AI capability. This dual-use structure is worth dwelling on: it means GE's AI investment is being amortized across two very different customer bases and two very different value propositions (margin for commercial airlines, readiness for the military) using largely the same underlying data architecture — a capital-efficiency advantage that a single-segment competitor wouldn't have.

2.4 The Competitive Read: This Becomes Table Stakes, Not a Durable Edge, Unless GE Moves Fast

Rolls-Royce and Pratt & Whitney are pursuing comparable predictive-maintenance and digital-twin capabilities, meaning GE's current advantage is more about execution speed and data scale (an installed base of well over 44,000 commercial engines in service) than about possessing a fundamentally unique technology. The open question industry analysts are already raising is whether airlines could eventually use their own or third-party AI diagnostic tools to extend shop-visit intervals independently of GE — though GE's LTSA billing structure, which charges per flight hour rather than per shop visit, blunts much of that specific risk for now. Section 4 below breaks this competitive picture out in more detail.

3. GE Aerospace Backlog Growth Timeline

The pace of backlog growth is itself a useful indicator of how much aftermarket demand GE's AI-driven efficiency push will eventually need to absorb and service:

| Reporting Period | Total Backlog | Commercial Services Backlog | Notable Context |

|---|---|---|---|

| Early-to-mid 2025 | [VERIFY: exact figure for this period] | ~$160B (per industry commentary) | Baseline widely cited in early-2026 analyst commentary |

| Q1 2025 (per company materials) | Over $170B (total equipment + services) | [VERIFY: segment breakdown for this period] | Cited as providing "exceptional long-term revenue visibility" |

| Full-year 2025 (as of Jan 22, 2026 release) | ~$190B | [VERIFY: exact commercial services figure at FY2025 close] | Grew ~$19–20B from previous year; full-year orders of $66.2B, +32% YoY |

| Q1 2026 (as of Apr 21, 2026 release) | ~$190B+ | $170B | Total orders of $23.0B in the quarter alone, +87% YoY |

| Entering Q2 2026 (per CFO commentary, mid-2026) | [VERIFY: updated total] | $170B (reaffirmed) | 95% of Q2 spare-parts revenue already locked into backlog before quarter began |

4. Competitive Landscape: Predictive Maintenance Across the Big Three Engine Makers

| Dimension | GE Aerospace | Rolls-Royce | Pratt & Whitney (RTX) |

|---|---|---|---|

| Primary AI partner/architecture | Palantir AIP / Foundry ("TrueChoice Defense" ecosystem) | [VERIFY: primary AI/digital-twin partner and platform name] | [VERIFY: primary AI/digital-twin partner and platform name] |

| Installed base scale | 44,000+ commercial engines in service | [VERIFY: current installed base figure] | [VERIFY: current installed base figure] |

| Reported predictive-maintenance impact | ~60% earlier fault detection; ~33% fewer unscheduled removals (Palantir Foundry rollout) | [VERIFY: comparable published figures, if any] | [VERIFY: comparable published figures, if any] |

| Revenue model underpinning aftermarket | LTSAs billed per flight hour, largely decoupled from shop-visit timing | [VERIFY: comparable service-contract structure] | [VERIFY: comparable service-contract structure] |

| Dual-use (commercial + defense) AI deployment | Yes — explicit commercial (CES) and defense (DPT) segments sharing underlying AI stack | [VERIFY] | [VERIFY] |

| Recent competitive pressure noted in market commentary | Reported to be "intensifying competitive pressure" on Raytheon/Pratt & Whitney's engine services segment per July 2026 market commentary | Investing in comparable capabilities per industry analysis | Facing pressure per the same commentary; competitive response reportedly underway |

The honest takeaway from this table is that GE's specific competitive edge is less about a proprietary AI capability Rolls-Royce or Pratt & Whitney fundamentally lack, and more about deployment scale and speed — GE's installed base and its early, expanding Palantir integration give it a head start in accumulating the fleet-wide sensor and maintenance-history data that any predictive-maintenance system depends on for accuracy, but that head start is time-limited rather than structural if competitors close the capability gap.

5. How This Fits the Broader Predictive Maintenance Trend

GE's specific numbers are worth placing against the wider aviation predictive-maintenance economics covered elsewhere on this blog, because they aren't outliers — they're consistent with what the broader industry is reporting. AOG events are estimated by Boeing to cost airlines anywhere from $10,000 to $150,000 per hour depending on aircraft type and route, with some industry sources citing average loaded AOG costs approaching $280,000 per event in 2026 once direct repair, labor premiums, and cascading schedule disruption are included. Separately, unscheduled labor is estimated to carry roughly a 3.2x cost premium over planned maintenance work, since every reactive hour effectively displaces two hours of productive, planned work. Against that backdrop, GE's reported 33% reduction in unscheduled engine removals isn't just an engineering metric — it's a direct lever on exactly the cost category (unscheduled, reactive maintenance) that the wider industry has identified as the single largest source of avoidable aftermarket cost. This is the same underlying economic logic explored in our companion domain pieces on Remaining Useful Life prediction and rare-failure-mode augmentation: the entire value proposition of predictive maintenance is converting unscheduled, expensive, reactive work into scheduled, cheaper, planned work, and GE's backlog economics make that conversion worth an estimated $500 million to $1 billion annually at their scale.

FLIGHT DECK, GE's internally branded lean operating system, is the less-discussed but arguably more important half of this story. Where the Palantir partnership provides the AI/data layer, FLIGHT DECK is the operational discipline layer GE credits with translating better data into better outcomes — the company's own materials describe FLIGHT DECK increasing material input from priority suppliers by more than 40% year-over-year in 2025, contributing directly to a 26% increase in commercial services revenue and a 25% increase in engine deliveries. GE's own 2025 annual report explicitly frames AI as an "accelerator for FLIGHT DECK" going into 2026 — worth noting because it reframes the AI narrative: GE isn't positioning AI as a replacement for operational discipline or lean manufacturing practice, but as a force-multiplier layered on top of an already-functioning operational system. This matters for anyone evaluating similar AI investments elsewhere in aerospace and defense — the GE case suggests predictive-maintenance AI delivers its strongest returns when paired with, rather than substituted for, disciplined operational execution.

Segment context also matters for interpreting where this AI investment pays off first. GE Aerospace reports across two segments — Commercial Engines & Services (CES), which contributes roughly three-quarters of total revenue, and Defense & Propulsion Technologies (DPT). The Palantir partnership's initial and most publicly detailed rollout has been on the defense side (T-38/J85 sustainment, broader Air Force readiness), while the larger dollar opportunity cited by analysts sits predominantly on the commercial CES side given its much larger revenue base and backlog. This suggests a plausible near-term trajectory: defense-sector deployment serving as the proving ground and pilot environment, with commercial-fleet-wide rollout as the larger, still-pending payoff — precisely the kind of "watch next" milestone flagged in Section 5 above.

| GE Aerospace Segment | Approx. Share of Total Revenue | Current AI/Palantir Deployment Status | Primary Value Driver |

|---|---|---|---|

| Commercial Engines & Services (CES) | ~75% | Broader digital-twin and predictive-maintenance tools in active use; full-scale Palantir integration less publicly detailed than defense side | Margin expansion on already-contracted LTSA revenue (est. $500M–$1B annually by 2028) |

| Defense & Propulsion Technologies (DPT) | ~25% | Most detailed public rollout — Palantir AIP across T-38/J85 sustainment, expanding "TrueChoice Defense" ecosystem | Fleet readiness — mission-capable aircraft rates, aircrew training throughput |

6. What to Watch Next

- Whether GE's Q2 2026 earnings (July 16, 2026) confirm the backlog and services-revenue trajectory continuing — CFO commentary already indicates 95% of Q2 spare-parts revenue was locked into backlog entering the quarter, a strong forward-visibility signal worth tracking against actual delivered results.

- Whether the Palantir partnership's predictive-maintenance architecture extends from the T-38/military pilot programs into GE's much larger commercial CFM56/LEAP fleet at scale, which is where the larger $500M–$1B margin opportunity cited by analysts would actually be realized rather than remaining a defense-sector proof of concept.

- Competitive responses from Rolls-Royce and Pratt & Whitney's own digital-twin and predictive-maintenance programs, since GE's current lead is time-limited if rivals close the capability gap — watch specifically for named platform announcements or published efficacy figures comparable to GE's 60%/33% numbers.

- Whether GE begins monetizing this AI capability directly as a software/SaaS offering to airline customers, as some analysts have speculated, rather than keeping it purely as an internal efficiency tool embedded in existing service contracts — this would be a meaningful business-model shift worth tracking closely.

- LEAP delivery bottleneck progress, since GE's own guidance flags breaking this bottleneck as a near-term execution priority — faster deliveries mean more engines entering the aftermarket pipeline sooner, directly affecting how quickly the backlog converts to recognized revenue.

- Whether independent, third-party validation of the 60% earlier detection / 33% fewer unscheduled removals figures emerges, since these numbers currently originate primarily from GE-affiliated and partner reporting rather than independently audited fleet-wide data — a natural next step for analysts seeking to stress-test the headline efficiency claims.

7. Anchor Data Point

GE Aerospace's predictive-maintenance work with Palantir has reportedly helped detect engine issues roughly 60% earlier and reduce unscheduled engine removals by about 33% — applied against a backlog that grew to nearly $190 billion in 2025, this is the specific mechanism by which AI is expected to convert an already-contracted revenue base into higher margin, not new market share.