Honeywell Forge: The Avionics Platform Bringing Predictive Analytics Beyond Jet Engines

Company Report: Honeywell Forge — The Avionics/Platform Alternative Bringing Predictive Analytics to APUs, Environmental Control Systems, and Avionics Fleet-Wide

1. Company Snapshot

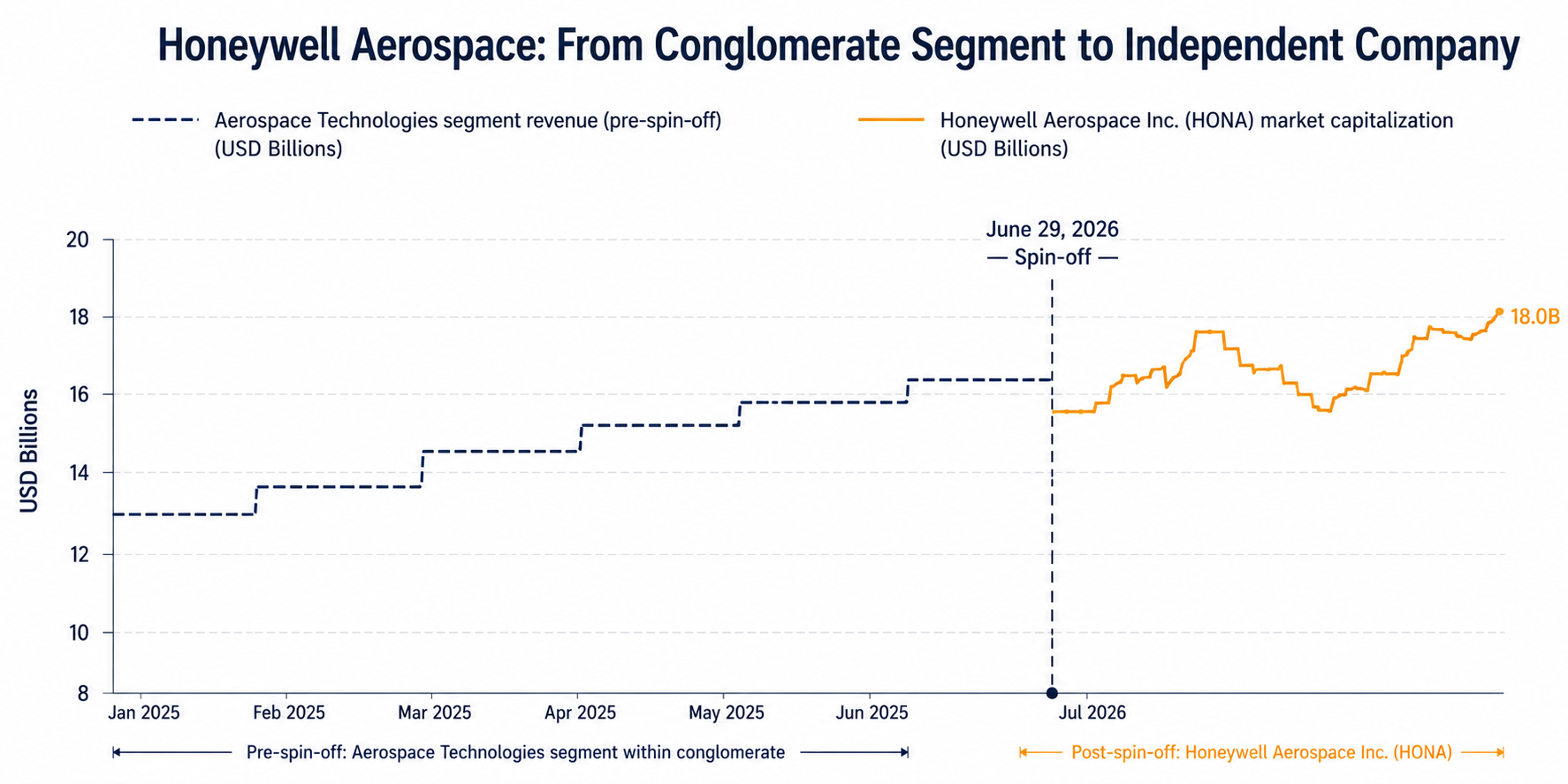

Honeywell Forge is the predictive-analytics software platform of Honeywell Aerospace — until very recently the Aerospace Technologies segment of the diversified Honeywell International conglomerate, and now, as of June 29, 2026, an independent, publicly traded company in its own right (Nasdaq: HONA). The spin-off is the final step of a multi-year breakup of Honeywell into three standalone public companies — Honeywell (industrial automation/building technologies), Solstice Advanced Materials, and Honeywell Aerospace — and it makes Honeywell Aerospace one of the largest pure-play, publicly traded aerospace suppliers in the world, with technology on virtually every commercial and defense aircraft platform. Where GE Aerospace and Safran's predictive-maintenance stories center on engines, Honeywell Forge's differentiated position is breadth across a different set of systems: auxiliary power units (APUs), environmental control systems, and integrated avionics — the "everything else" on the aircraft that also fails, delays flights, and generates its own large maintenance bill.

| Attribute | Detail |

|---|---|

| Founded | Aerospace heritage traces to 1914 (Honeywell Aerospace's predecessor businesses, including the invention of the first autopilot); spun off as an independent public company on June 29, 2026 |

| HQ | Phoenix, Arizona, United States |

| Founders/CEO | Spun off from Honeywell International Inc. (Chairman & CEO Vimal Kapur); current President & CEO of Honeywell Aerospace: Jim Currier |

| Total Funding | Not applicable in the venture sense — Honeywell Aerospace is a corporate spin-off, distributed to existing Honeywell shareholders (one HONA share for every two Honeywell Technologies shares held as of June 15, 2026); no disclosed private/VC funding |

| Latest Valuation (Market Cap) | Approximately $66–71B as of mid-July 2026 <br>[VERIFY: exact figure on date of publication, as this moves daily with the share price] |

| Employee count | More than 36,000 at spin-off (some third-party trackers report ~30,000; treat the company's own press release figure as authoritative) [VERIFY: current headcount] |

2. What They Actually Build

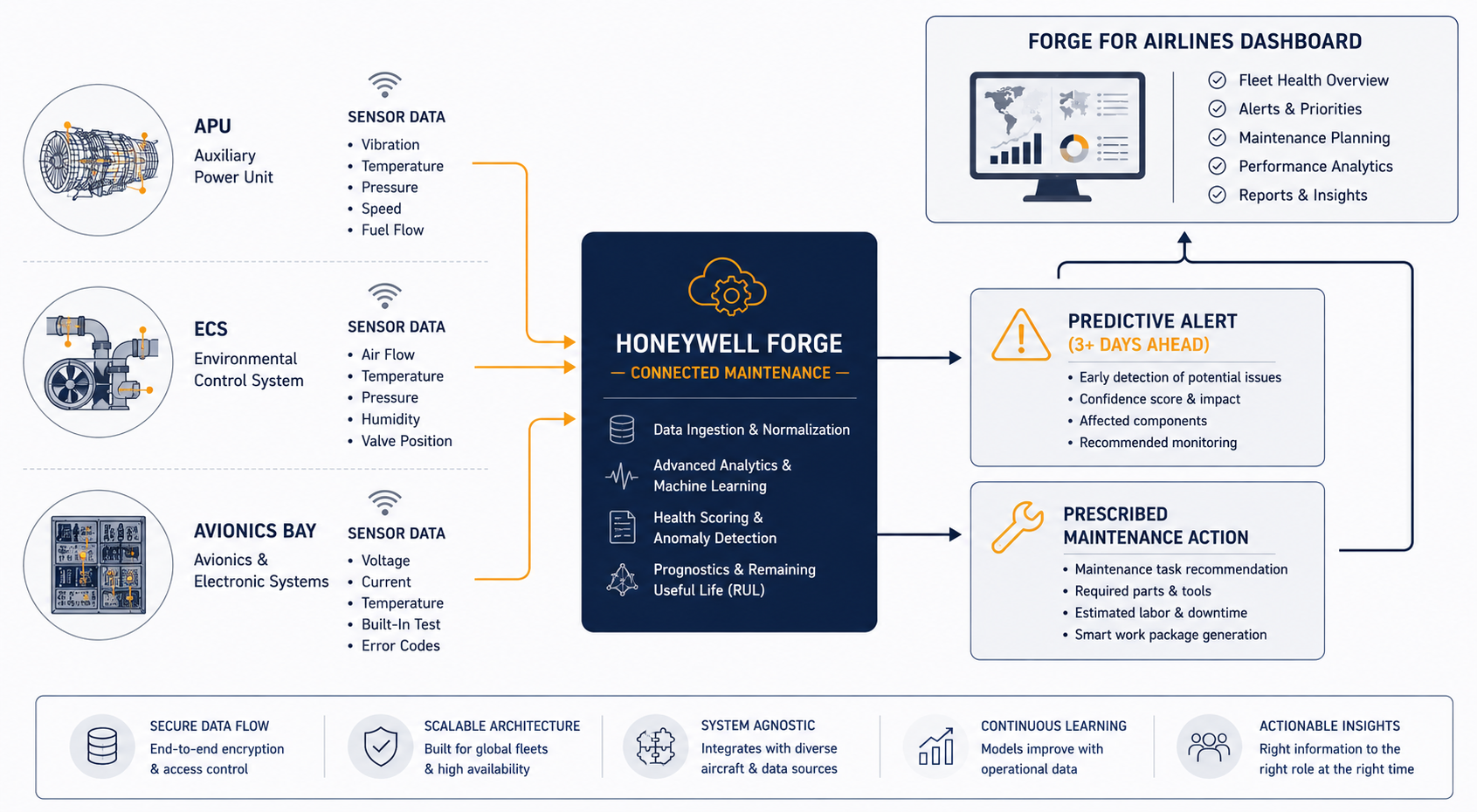

Honeywell Aerospace's hardware portfolio spans propulsion (APUs and business/regional jet engines), cockpit and navigation systems (integrated avionics, flight safety, communications, radar and surveillance), auxiliary and electric power systems, engine controls, connectivity services, and aircraft wheels, brakes, and thermal systems — plus a substantial spare parts, repair, and MRO services business layered on top of all of it. Honeywell Forge is the software and analytics layer that sits across this hardware portfolio, and it is best understood as several distinct applications bundled under one platform brand rather than a single monolithic product:

- Connected Maintenance (built on the legacy PTMD — Predictive Trend Monitoring and Diagnostics — application) ingests aircraft condition monitoring system (ACMS) data, QAR flight data, fault messages, and maintenance tech logs to generate predictive alerts and prescribed maintenance actions across more than a dozen ATA chapters, with APU monitoring (ATA Chapter 49) as its original and most mature use case, built on a training base of more than 100 million service hours for its most widely deployed APU model alone.

- Forge Performance+ for Aerospace, introduced in April 2024, combines predictive maintenance, site optimization, and workforce intelligence into a single cloud-based platform aimed at MRO facilities and aerospace manufacturing operations, not just airline flight-line maintenance.

- Forge for Airlines is the unified front-end that consolidates flight operations, flight efficiency, and connected maintenance applications into one interface for airline customers, layering cognitive diagnostics (machine-learning-assisted troubleshooting) and wireless data transfer on top of the underlying predictive models.

The company's own published performance figures for Connected Maintenance on APUs are specific and worth stating plainly rather than paraphrased into vaguer language: airlines using the system have reported a 30–50% reduction in APU-related operational disruptions, a 10–15% reduction in costly premature removals, a no-fault-found rate reduced to roughly 1.5%, and a claimed 99% predictive accuracy — with failure alerts typically generated at least three days ahead of the predicted event. A published Cathay Pacific case study is the most granular public example: across 61 aircraft, Forge analyzed 1.6 million flight records, 327,000 maintenance entries, 44,000 fault messages, and 13,000 APU reports, and the airline reported a 30% reduction in delays and cancellations and a 90% reduction in repair times as a result.

| Forge Component | What It Covers | Notable Disclosed Result |

|---|---|---|

| Connected Maintenance / PTMD | APU and broader ATA-chapter predictive diagnostics | 30-50% fewer APU disruptions; 99% predictive accuracy |

| Forge Performance+ for Aerospace | MRO facility and manufacturing operations optimization | Combines predictive maintenance with site/workforce analytics |

| Forge for Airlines | Unified flight ops + maintenance + efficiency interface | Cathay Pacific: 30% fewer delays/cancellations, 90% faster repairs |

3. Recent Moves (Last ~6–12 Months)

The past year has been the most consequential in Honeywell Aerospace's corporate history, dominated by the completion of its spin-off, alongside continued product and partnership activity around Forge itself.

The three-way Honeywell breakup and Aerospace spin-off (February 2025 – June 2026). Honeywell announced on February 6, 2025 that it would split its automation and aerospace divisions into two separate public companies, alongside the already-announced Solstice Advanced Materials spin-off — resulting in three independent, publicly traded companies in total. The Aerospace spin-off itself was completed on June 29, 2026, when Honeywell Technologies distributed one share of Honeywell Aerospace common stock for every two Honeywell Technologies shares held as of the June 15, 2026 record date. Honeywell Aerospace began trading on Nasdaq under "HONA" that day and was almost immediately added to both the S&P 500 and S&P 100 indices, replacing Conagra Brands and Honeywell International, respectively.

A defense avionics contract win drove a sharp share-price move (early July 2026). HONA shares reportedly rose as much as 7.82% after the company secured a multi-year defense avionics upgrade contract. [VERIFY: specific customer/platform named in the contract, and confirmed award value]

An Odysight.ai proof-of-concept for vision-based APU monitoring (June 18, 2026). Honeywell's APU division issued a purchase order to Odysight.ai (Nasdaq/TASE: ODYS) to evaluate a vision-based predictive maintenance sensing platform across Honeywell's APU portfolio — an installed base described as more than 10,000 units — initially focused on the APU air intake, a location prone to debris, icing, and contamination that's historically hard to inspect visually.

An MOU with Enigma Aerospace. Honeywell Aerospace and Enigma Aerospace signed a memorandum of understanding to explore integrating their respective capabilities. [VERIFY: specific scope of the collaboration, which was not detailed in available public reporting at the time of this report]

Early analyst coverage was mixed but constructive. Wolfe Research initiated HONA at a neutral "Peer Perform" rating, JPMorgan initiated at "Neutral," and Argus initiated at "Buy" with a $275 price target — reflecting a market still forming a consensus view on a newly independent company carrying a levered balance sheet (roughly $15.8B in long-term debt at spin-off) alongside strong operating margins (mid-teens EBIT margin, ~18.4% pretax margin in its first reported quarter as a standalone entity).

4. Competitive Position

Honeywell Aerospace's Forge platform competes across three distinct system categories, each with a somewhat different competitive landscape, which is worth naming explicitly rather than treating "Honeywell's competitor" as a single answer. In avionics and cockpit systems, its most direct named peer is Collins Aerospace, a Raytheon Technologies (RTX) business; in engines (including APUs, where Honeywell holds a historically dominant position), GE Aerospace and Safran are the more relevant comparators, though neither is a like-for-like APU competitor at Honeywell's scale.

| Dimension | Honeywell Aerospace (Forge) | Collins Aerospace (RTX) |

|---|---|---|

| Core system focus | APUs, environmental control systems, integrated avionics, engine controls, connectivity | Avionics, cabin interiors, mechanical systems, actuation, communication/navigation |

| Corporate structure | Newly independent standalone public company (spun off June 2026) | Business unit within the larger RTX Corporation, alongside Pratt & Whitney |

| Predictive maintenance branding | Named, publicly quantified platform (Honeywell Forge / Connected Maintenance) with disclosed performance metrics (99% predictive accuracy, 30-50% fewer APU disruptions) | Investing in comparable connected-aircraft and predictive analytics capability; less granular public disclosure of platform-specific performance metrics as of this writing [VERIFY] |

| Installed base scale (APU-specific) | More than 10,000 Honeywell APUs referenced in a recent third-party partnership announcement; one APU model alone has more than 100 million service hours of data | [VERIFY: Collins Aerospace APU/avionics installed base figures, where applicable] |

| 2025 annual revenue | More than $17B (Aerospace Technologies segment, pre-spin-off) | [VERIFY: Collins Aerospace segment-specific revenue, as RTX reports it within a larger corporate structure] |

The practical takeaway: Honeywell Aerospace's Forge platform is less a head-to-head "GE Aerospace but for avionics" story and more a genuinely adjacent business line — its predictive-maintenance value proposition is concentrated specifically on the systems (APUs, ECS, avionics) that engine-focused competitors like GE Aerospace and Safran largely don't address, which is precisely the "platform alternative" framing in this report's title. Where it does compete head-on with Collins Aerospace, in avionics and cockpit systems specifically, the newly independent balance sheet and capital-allocation freedom Honeywell Aerospace's leadership has emphasized post-spin-off is a variable worth watching, since Collins Aerospace continues to operate within RTX's broader capital allocation priorities rather than as a standalone entity.

5. Why It Matters

Honeywell Forge matters to the broader defense-AI industry for a reason distinct from the GE Aerospace story: it demonstrates that predictive-maintenance AI creates real, quantified value even on systems that don't get the same attention as jet engines — APUs, environmental control systems, and avionics boxes are individually less glamorous than a turbofan, but collectively they drive a very large share of airline delays, cancellations, and no-fault-found removals, and Honeywell's own published figures (a 1.5% no-fault-found rate, 99% predictive accuracy, 90% faster repairs in the Cathay Pacific case) suggest this "unglamorous systems" category may have been comparatively under-invested relative to its actual impact on fleet availability. It also matters as a structural signal: Honeywell Aerospace's spin-off into a standalone, S&P 500-listed public company gives outside analysts and competitors a clean, segment-specific financial window into a predictive-maintenance business for the first time — something that was previously blended into a much larger conglomerate's reporting — which should, over the next few quarters, make it considerably easier to benchmark AI-driven maintenance economics against GE Aerospace's comparable disclosures.

6. Chart Data Table

(Note: Honeywell Aerospace is a public corporate spin-off, not a venture-funded company — there are no priced equity funding rounds in the traditional startup sense. The table below is adapted to track the corporate and market milestones most relevant to this report's thesis: the path from conglomerate segment to independent, Forge-branded public company.)

Funding Timeline Data (Adapted: Corporate Separation & Market Cap Timeline)

| Milestone | Date | Segment/Company Revenue ($B) | Market Capitalization ($B) |

|---|---|---|---|

| Honeywell announces 3-way portfolio split | February 6, 2025 | ~$15B (2024 Aerospace Technologies revenue, as reported at announcement) | N/A (still part of Honeywell International) |

| Full-year 2025 Aerospace Technologies revenue reported | ~Early 2026 | >$17B | N/A (pre-spin-off) |

| Spin-off record date | June 15, 2026 | N/A | N/A |

| Honeywell Aerospace begins independent trading (Nasdaq: HONA) | June 29, 2026 | N/A | ~$71B (initial trading) |

| S&P 500 / S&P 100 inclusion | June 29–30, 2026 | N/A | ~$71B |

| Latest available market cap | July 14, 2026 | N/A | ~$66B [VERIFY: exact figure on publication date] |