Low Earth Orbit Is Getting Crowded — and That's Creating a New AI Market

Space used to feel practically empty. That's no longer true, and the numbers behind that shift are the real reason an entire new category of AI companies — space domain awareness (SDA) providers — has emerged and is growing fast heading into 2027.

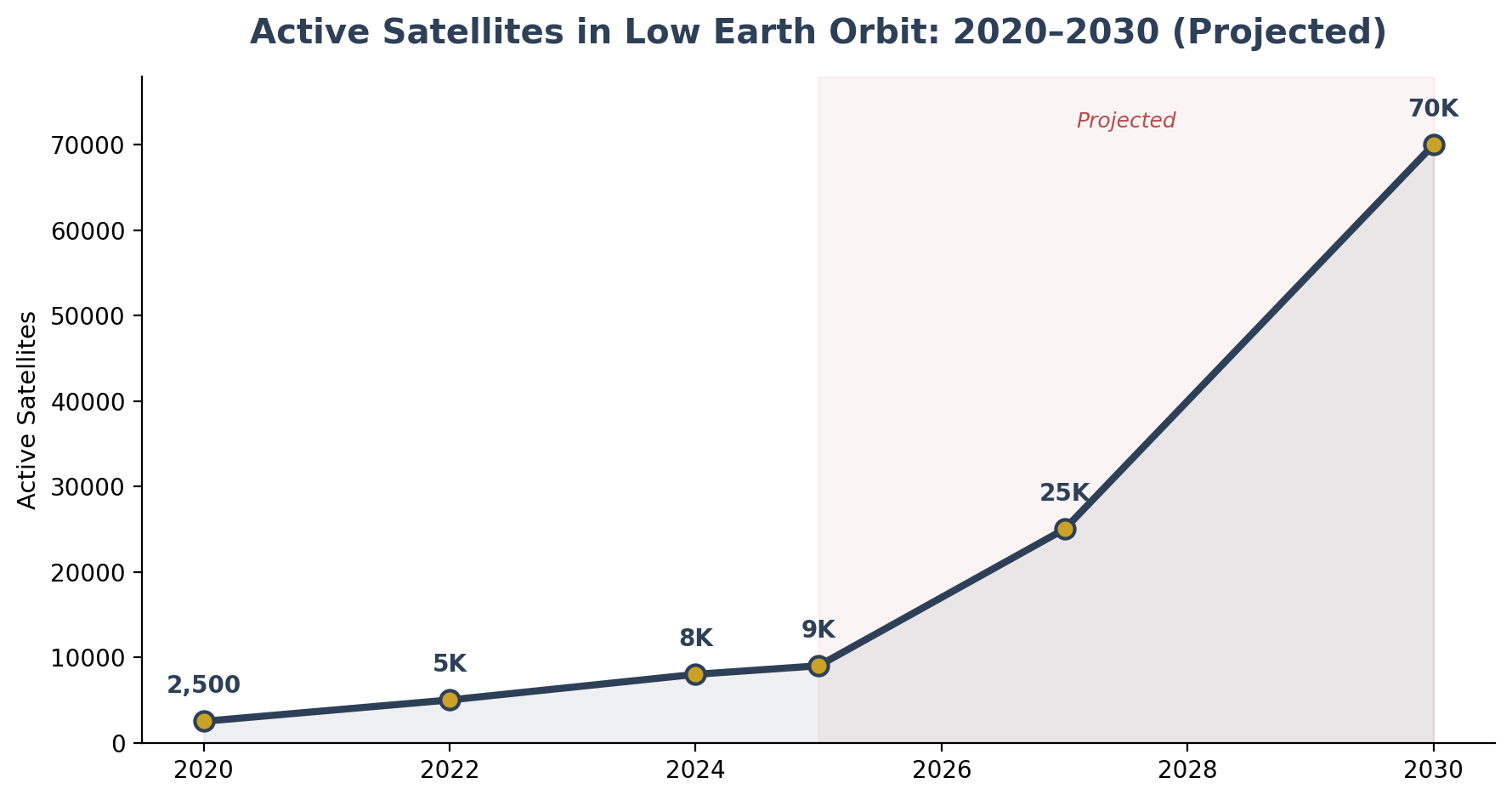

1. How crowded is "crowded," actually?

By 2025, more than 9,000 active satellites were operating in low Earth orbit, accounting for roughly three-quarters of all active satellites globally — up sharply from a much smaller number just five years earlier. Industry forecasts commonly cited by SDA companies (including LeoLabs, covered elsewhere in this series) project the number of operational satellites in LEO could exceed 70,000 by 2030, driven largely by commercial mega-constellations from companies like SpaceX, Amazon, and others.

Satellites aren't the only thing up there. Surveillance networks track roughly 40,000 objects in orbit today, but that figure only includes things large enough to detect reliably — debris smaller than about 10 centimeters, estimated to number well over a million fragments, is largely untracked but still fast-moving and dangerous enough to destroy a satellite on impact. This is the core of what's known as the Kessler syndrome risk: the more objects are up there, the more collisions occur, and each collision creates more debris, which raises the odds of further collisions.

2. Why this creates an actual, provable business problem

More objects means more risk of collision, which means every satellite operator now has to spend real money and engineering effort just to stay safe:

Regulators have tightened the rules. The FCC now requires LEO satellite operators to deorbit their satellites within five years of the end of their mission, replacing a much looser 25-year guideline that used to apply. Compliance with this kind of rule requires accurate tracking, planning, and reporting — not something a small satellite operator can easily do without outside tools.

Every close approach needs to be checked and, if necessary, avoided. Satellite operators increasingly report needing to perform more frequent collision-avoidance maneuvers simply because of how many other objects are nearby — each maneuver costs fuel, which is a limited, non-renewable resource on any given satellite, directly shortening its useful working life.

Insurance and launch licensing now factor in orbital congestion. As the environment gets riskier, insurers and regulators are scrutinizing debris mitigation plans and collision risk more closely before approving launches or insuring satellites — adding cost and complexity that didn't exist a decade ago.

3. This is exactly why AI-powered SDA is now a real market category

None of this can be handled by a human team checking a spreadsheet. With tens of thousands of tracked objects and millions of potential close-approach events to evaluate, only automated, AI-assisted systems can realistically process the volume of tracking data involved and flag what actually matters. That's the specific gap companies like Slingshot Aerospace and LeoLabs — both covered in depth elsewhere in this series — are building businesses around: turning raw orbital tracking data into automated, actionable alerts.

Multiple independent market research firms estimate the global space situational awareness (SSA) market at somewhere between roughly $1.7 billion and $2.3 billion in 2026, with most forecasts projecting steady growth (commonly cited growth rates fall in the 4–10% CAGR range depending on the research firm) through the early 2030s as orbital congestion continues to worsen. It's worth noting plainly that different market research firms report meaningfully different size and growth figures for this market — a common issue with any young, fast-moving industry category — so these numbers should be read as directional estimates, not precise figures.

North America currently holds the largest share of this market, driven heavily by U.S. Space Force investment in radar networks, AI analytics, and real-time tracking, while the Asia-Pacific region is forecast to grow the fastest, driven by rapid satellite deployment from India, Japan, South Korea, and China.

4. Why this matters beyond the satellite industry itself

This trend is a useful, concrete example of a broader pattern in defense and commercial AI: when a physical environment gets too complex and fast-moving for humans to monitor manually, an AI-driven monitoring and decision-support market almost always emerges to fill that gap. The same underlying pattern — too much data, too many objects, too little time for a human to process it all manually — shows up in air traffic control, maritime shipping-lane monitoring, and cybersecurity network monitoring, not just orbit.

Orbital congestion isn't a problem that's going away — every forecast points toward more satellites, not fewer, over the next decade. That makes space domain awareness one of the more durable, structurally growing corners of defense AI heading into the rest of this decade, rather than a short-term trend tied to any single company's product cycle.

Sources: Fortune Business Insights; MarketsandMarkets; Grand View Research; Coherent Market Insights; Business Research Insights; European Space Agency Space Environment Report; FCC orbital debris rules. Market size figures vary meaningfully across research firms and are presented here as estimates, not precise values.