Resilient PNT: The Emerging Market for GPS-Independent Navigation

Resilient PNT: The Emerging Market for GPS-Independent Navigation

Chip-scale atomic clocks, LEO-PNT constellations, and celestial navigation are no longer backup slides in a risk briefing — they're becoming line items in defense budgets and venture term sheets.

1. What Happened

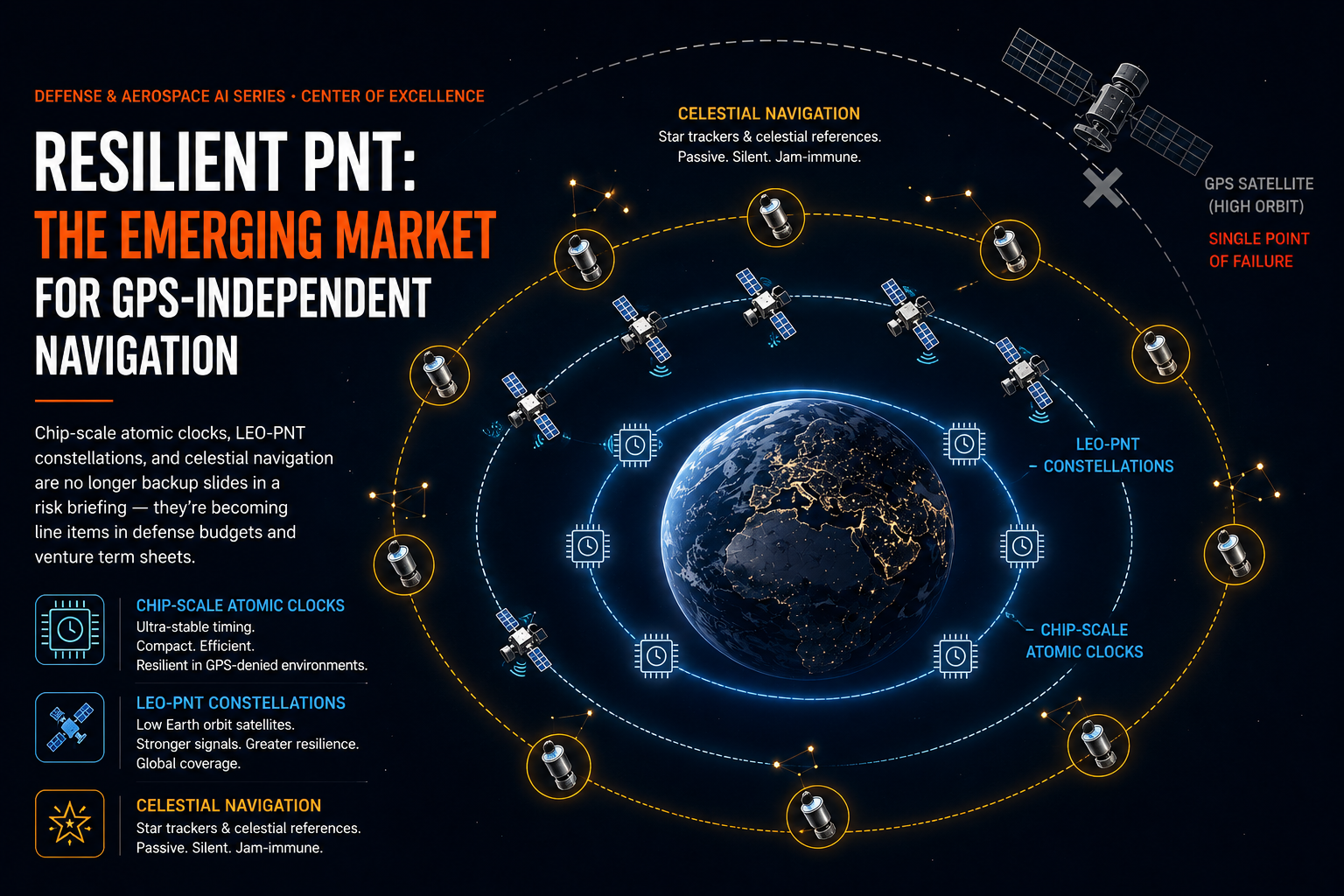

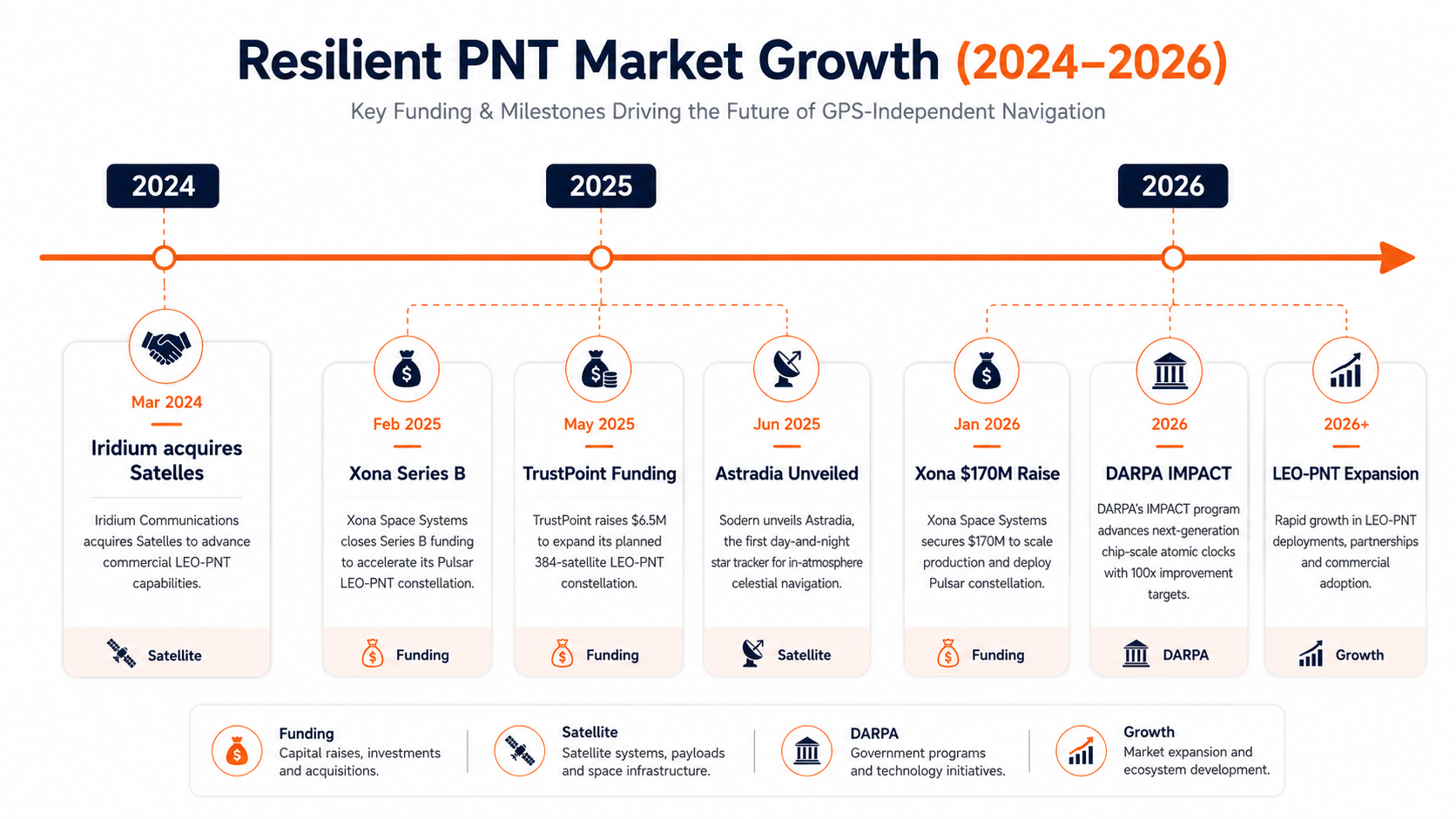

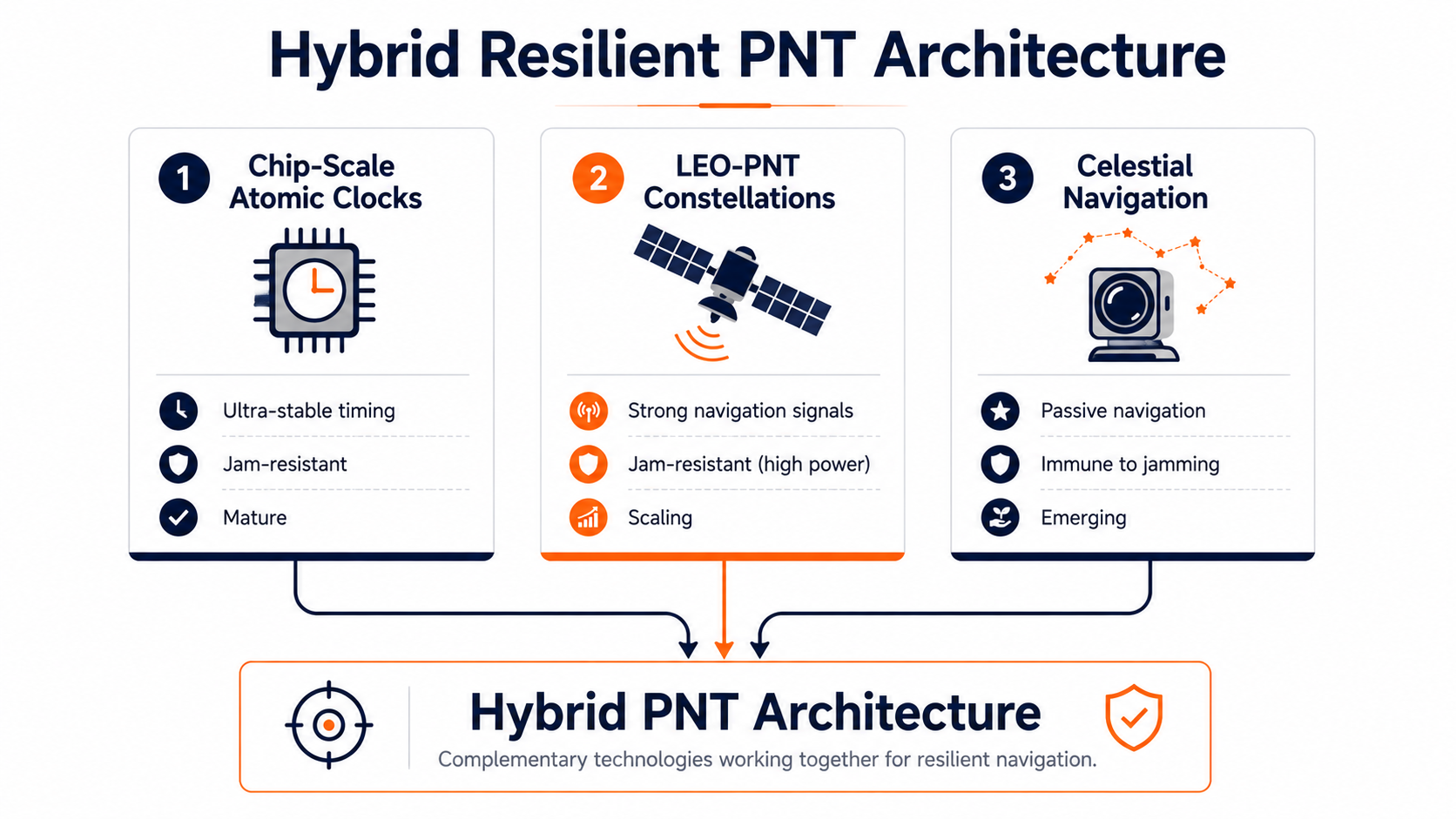

Three previously niche navigation technologies — chip-scale atomic clocks (CSAC), low Earth orbit positioning-navigation-timing (LEO-PNT) constellations, and modern celestial (star-tracker) navigation — have moved from research-lab curiosities to funded, contracted, and in some cases operationally deployed products across 2025–2026. Xona Space Systems closed a $170 million raise for its Pulsar LEO-PNT constellation; Iridium's Satelles-derived STL (Satellite Time and Location) service and Sodern's Astradia star tracker have both moved into fielded or near-fielded status; and DARPA's chip-scale atomic clock lineage continues to fund next-generation miniaturized timing.

2. Why It Matters

The core driver behind all three of these technology tracks is the same one covered in our companion piece on the 2026 Baltic and Middle East GNSS-jamming crisis: GPS/GNSS is a single, structurally fragile point of failure, and the market has stopped waiting for that to be fixed at the source. What's changed recently isn't the threat — jamming and spoofing have been documented for years — it's that capital, contracts, and defense procurement decisions are now organizing around three distinct, complementary technical answers rather than one.

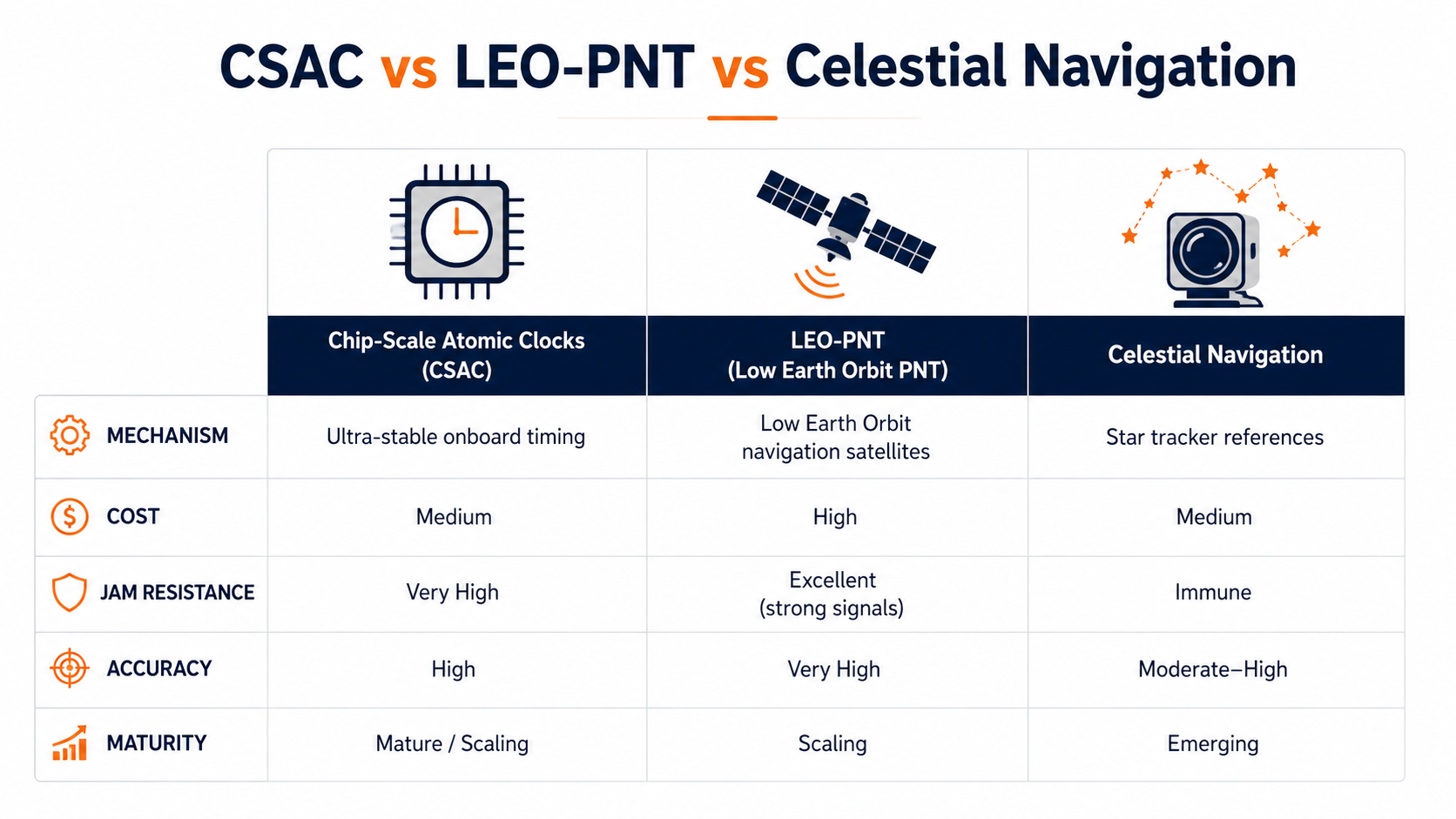

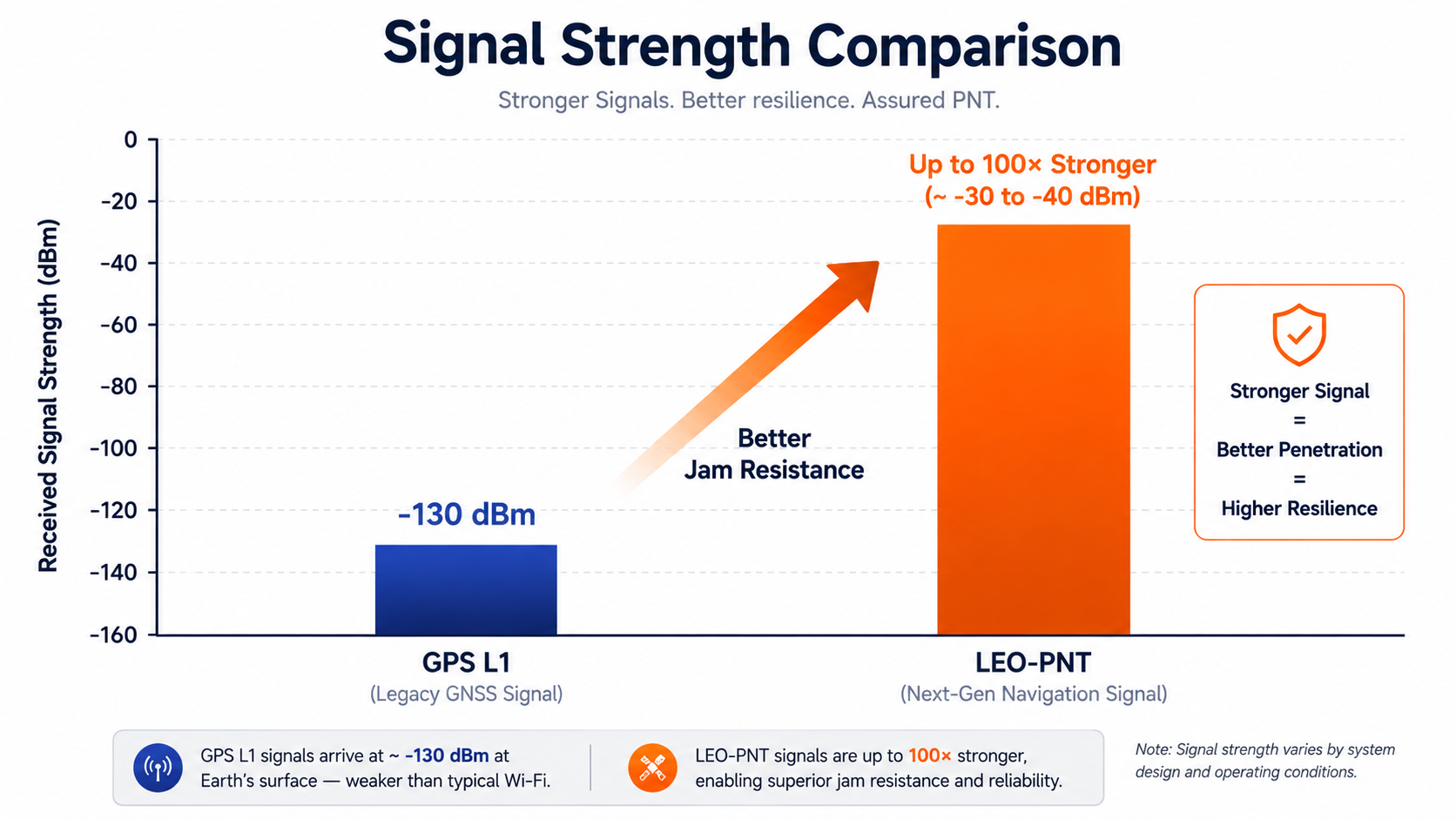

LEO-PNT is the most capital-intensive and the most contested track. Xona's Pulsar constellation, operating at roughly 1,080 km altitude, is designed around a core physical advantage: because LEO satellites sit dramatically closer to Earth than GPS's medium-Earth-orbit altitude, their signals can arrive up to 100 times stronger, which directly translates into far greater jam resistance and better indoor/urban penetration. The company's Pulsar-0 demonstrator has already shown 42-millimeter on-orbit accuracy, and Xona is targeting a 258-satellite constellation with first U.S. launches in 2026. It isn't alone: TrustPoint has raised smaller sums (around $6.5 million) toward a planned 384-satellite constellation, and Iridium — after acquiring Satelles for approximately $115 million in 2024 — now operates the STL service, which multiple industry trackers describe as the only fully operational commercial LEO-PNT service as of late 2025. Worth flagging for anyone evaluating this space: published market-size estimates for LEO-PNT vary enormously between research firms — from roughly $154 million in 2026 growing at a 32% CAGR, to alternative estimates spanning $70–90 million growing at over 50% CAGR — a spread that says more about how immature and undefined this market category still is than it does about any single number being "right."

CSAC is the quieter, more mature, but still-scaling track. Chip-scale atomic clocks trace their lineage directly to a DARPA program that achieved a hundredfold size reduction and fiftyfold power reduction versus legacy atomic clocks, enabling jam-resistant GPS receivers and secure military communications; commercial manufacturing began in 2011, and today Microchip (formerly Microsemi), Teledyne, Chengdu Spaceon, Orolia (part of Safran), and Frequency Electronics are the recognized commercial players. DARPA's follow-on IMPACT program is targeting a further two-orders-of-magnitude improvement in accuracy and stability. As with LEO-PNT, published CSAC market-size figures diverge sharply across research firms — estimates for the current global or U.S. market range from tens of millions to well over a billion dollars depending on scope and methodology — but the qualitative signal across every source is consistent: demand is being pulled by GPS-denied navigation requirements, 5G/6G synchronization, and defense procurement, not by any single application alone.

Celestial navigation is the smallest but most conceptually striking comeback story. Sodern, an ArianeGroup subsidiary, unveiled Astradia — described as the first operational sensor of its kind capable of star-tracking navigation during both day and night from inside the atmosphere — at the 2025 Paris Air Show, explicitly targeting military aircraft first before civil applications. Honeywell has productized a comparable capability, Celestial Aided Navigation (CNAV), as one layer within its broader Alternative Navigation Suite, and Draper Laboratory holds a patented "sliced-lens" star tracker design already demonstrating 50-meter-class accuracy in GNSS-denied conditions. None of these claim to replace GPS-grade accuracy outright; their value proposition is entirely about being passive, signal-free, and therefore immune to jamming or spoofing by construction, which is precisely the property regulators and militaries are now willing to pay a premium for.

The strategic read for a Center of Excellence: these three tracks are not competing for the same procurement dollar — they're complementary layers in what nearly every major prime and agency now calls a "multi-layer" or "hybrid" PNT architecture, and the companies best positioned aren't necessarily the ones with the single best technology, but the ones building sensor-fusion products that blend two or three of these layers together.

3. What to Watch Next

Xona's first U.S. Pulsar launches in 2026 and whether the company hits its stated pace of producing more satellites per week than the U.S. government currently builds navigation satellites annually — a claim that, if true, would be a meaningful manufacturing-scale signal for the whole LEO-PNT category.

Whether TrustPoint or other second-tier LEO-PNT entrants close a Xona-scale funding round, which would suggest the category is broadening beyond a single dominant player.

DARPA's IMPACT program progressing toward its stated 20 cm³, sub-160-nanosecond-drift target, which would meaningfully compress size, weight, and power budgets for CSAC-equipped platforms.

Whether Sodern's Astradia or Honeywell's CNAV secure a named platform integration or certification milestone — moving from "unveiled" to "flying operationally" is the next credibility threshold for celestial navigation.

Consolidation activity, given the pattern already set by Iridium's acquisition of Satelles — expect further primes or satellite operators to acquire smaller PNT startups rather than build competing capability organically.

4. Anchor Data Point

A standard GPS L1 signal arrives at Earth's surface at roughly -130 dBm — weaker than a typical Wi-Fi signal — while LEO-PNT systems like Xona's Pulsar are designed to deliver signals up to 100 times stronger from orbit. That single physical difference is the entire commercial thesis behind the LEO-PNT market.