The Digital Twin Race in MRO: GE, Rolls-Royce, and Pratt & Whitney's Competing AI Strategies

The Digital Twin Race in MRO: GE, Rolls-Royce, and Pratt & Whitney's Competing AI Strategies

All three engine makers are chasing the same prize — fewer unscheduled removals, more time on wing — but they're building fundamentally different digital architectures to get there.

1. What Happened

The three companies that build the vast majority of the world's commercial jet engines — GE Aerospace, Rolls-Royce, and Pratt & Whitney (a division of RTX) — have each spent the past several years building out named, branded digital-twin and AI-driven predictive-maintenance platforms: GE's Palantir-powered architecture (most recently expanded into a "TrueChoice Defense" ecosystem in March 2026), Rolls-Royce's IntelligentEngine and Blue Data Thread initiative (built with IFS Maintenix since 2019), and Pratt & Whitney's EngineWise platform built around its ADEM (Advanced Diagnostics and Engine Monitoring) system. Each company has published its own efficiency figures, and each is racing to convert a multi-decade installed base of engines into a lower-cost, higher-margin aftermarket services business using AI.

2. Why It Matters

2.1 The Shared Economic Logic Behind All Three Strategies

Before comparing the three approaches, it's worth being clear about why every major engine maker is making this same bet simultaneously. Modern jet engines are sold under long-term service agreements (LTSAs) that generate a 25–30 year aftermarket revenue stream per engine, typically billed per flight hour regardless of exactly when a shop visit occurs. This means the engine makers' aftermarket profitability depends almost entirely on how efficiently they can deliver that decades-long service commitment — catching problems early, scheduling shop visits precisely, avoiding unscheduled removals, and keeping spare-parts inventory lean. Digital twins and AI-driven diagnostics attack exactly this cost structure, which is why all three companies are pursuing structurally similar strategies even though their specific technical architectures differ meaningfully, as detailed below.

2.2 GE Aerospace: The Palantir-Powered, Dual-Use Approach

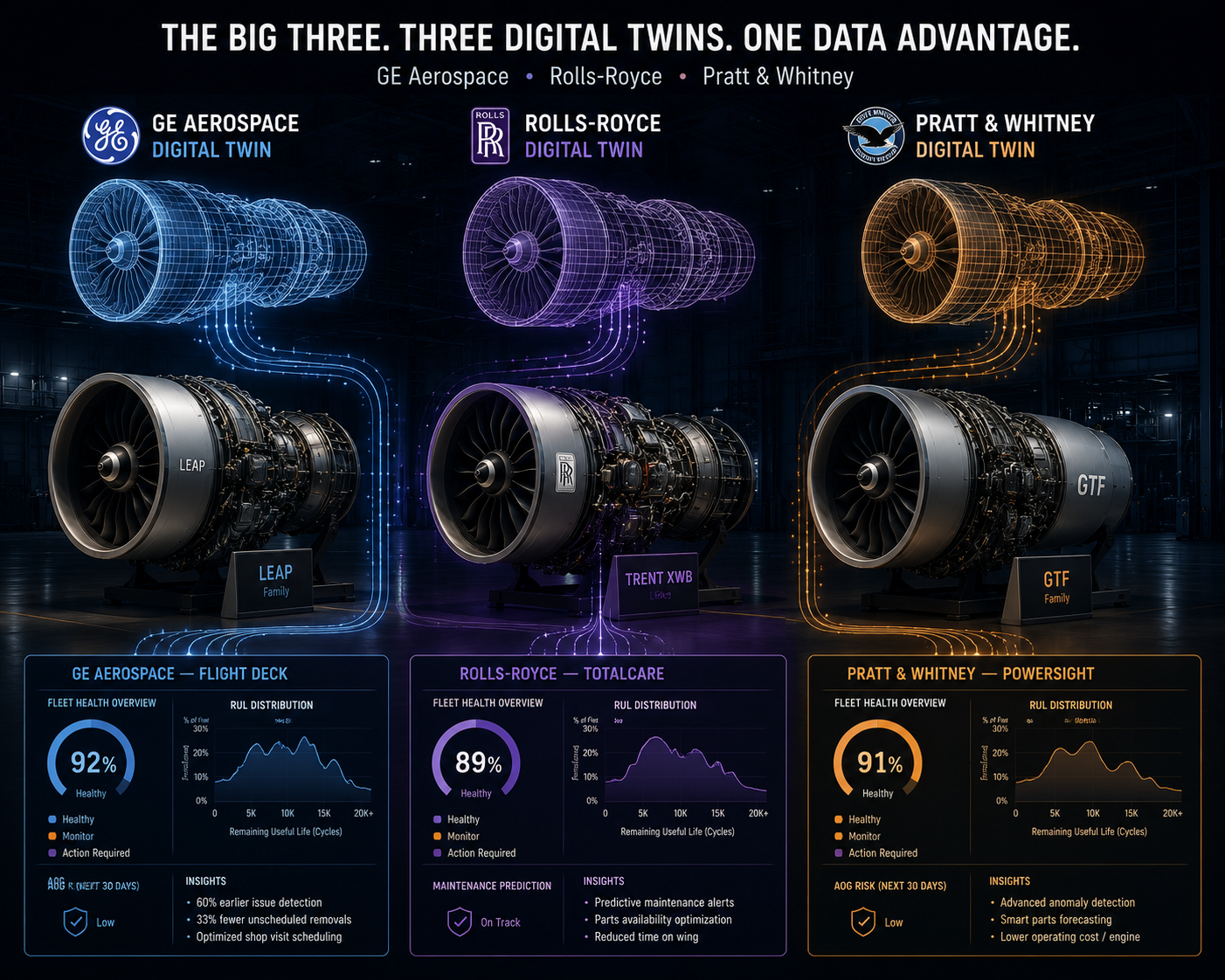

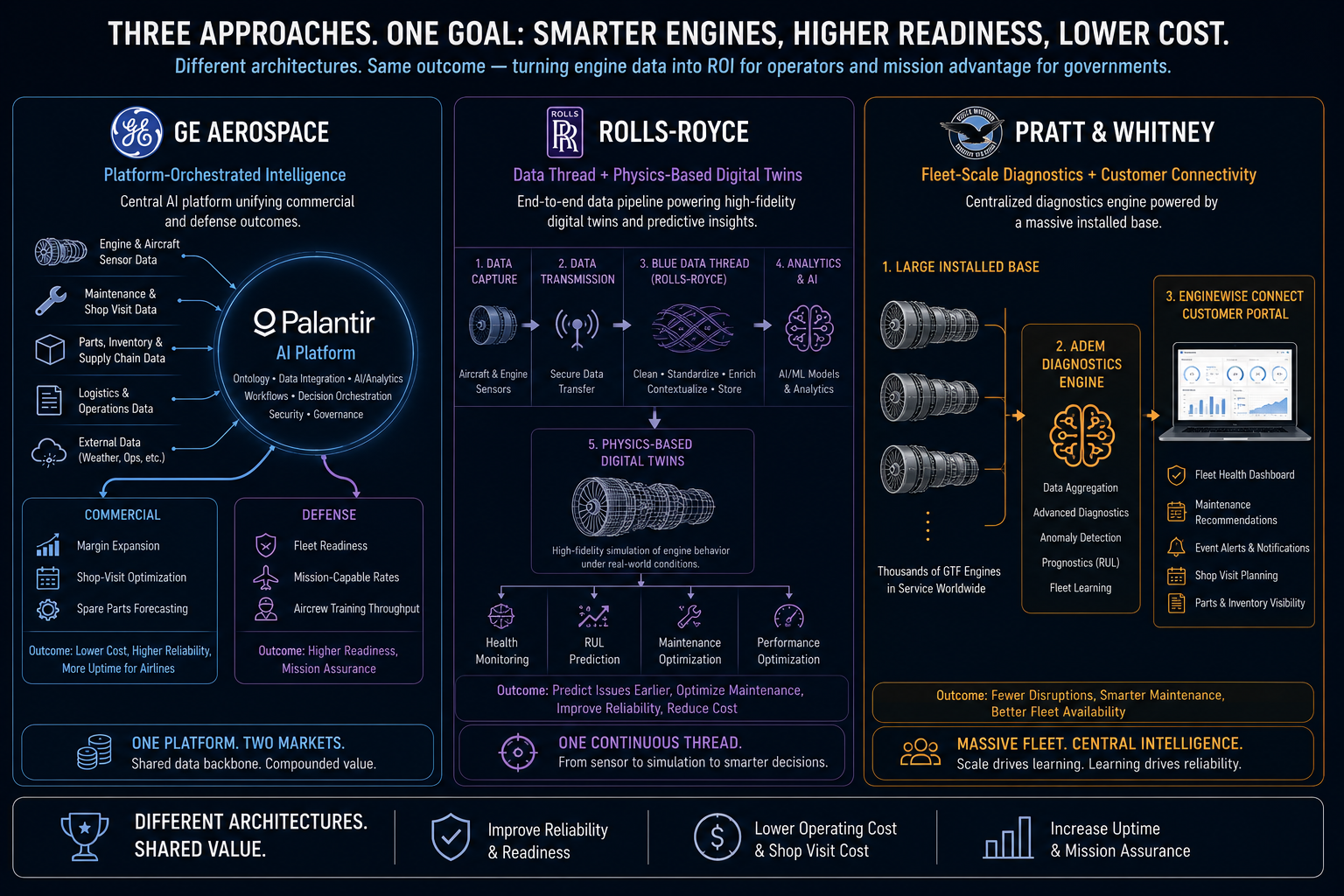

GE's strategy, covered in more depth in our companion piece on GE's AI-driven predictive maintenance push, centers on a deepening partnership with Palantir Technologies, using Palantir's AIP (Artificial Intelligence Platform) and Foundry software to unify data across fulfillment, sourcing, allocation, maintenance, repair, and customer service. What distinguishes GE's approach from its two rivals is its explicit dual-use structure: the same underlying AI architecture serves both GE's commercial aftermarket business (targeting an estimated $500 million to $1 billion annual margin opportunity by 2028) and its defense sustainment work with the U.S. Air Force (currently centered on T-38/J85 engine readiness, under the "TrueChoice Defense" branding). Reported results from GE's broader Palantir Foundry rollout include detecting engine issues roughly 60% earlier and reducing unscheduled engine removals by around 33%. GE's approach is also the most visibly tied to a single external software partner — a structural choice that concentrates capability quickly but also creates a degree of vendor dependency not present in the other two companies' more internally built architectures.

2.3 Rolls-Royce: The Longest-Running, Most Architecturally Mature Program

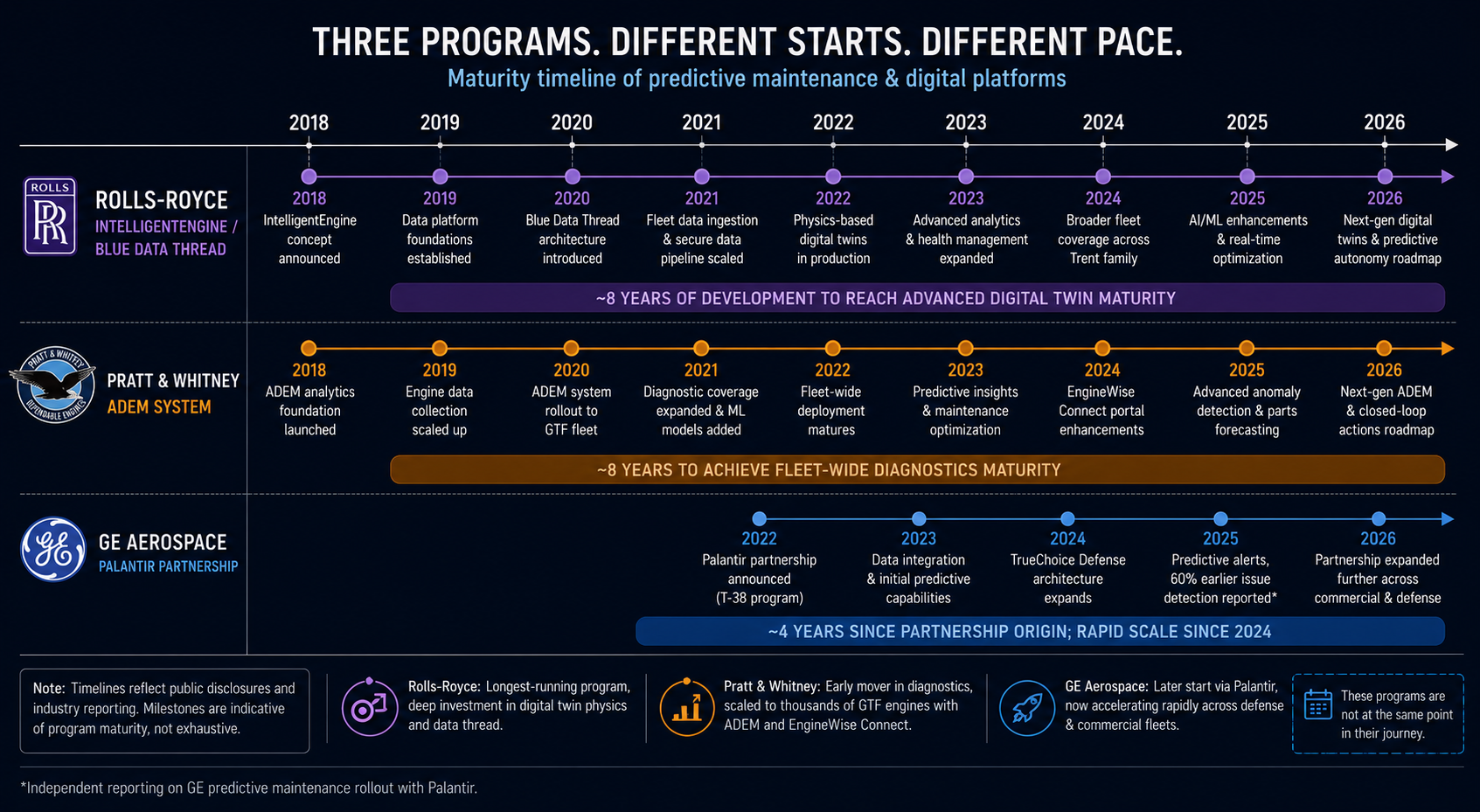

Rolls-Royce's IntelligentEngine initiative predates both of its rivals' current AI pushes by several years — the program traces back to a 2018–2019 partnership with IFS to build the "Blue Data Thread," a digital information thread explicitly designed to connect every Rolls-Royce-powered aircraft, airline operation, maintenance shop, and factory into a single data pipeline. This is a meaningfully different architectural philosophy from GE's platform-partnership model: rather than layering a single external AI platform on top of existing operations, Rolls-Royce built its digital twin capability around continuous, automated data capture directly from customers (replacing an earlier, more manual process where airlines periodically uploaded spreadsheets of engine usage data), feeding physics-based digital twins of specific engine families — the Trent 1000, Trent XWB, and Trent 7000 among them. Rolls-Royce has also brought in cloud and IoT infrastructure partners including Microsoft Azure and Siemens to scale this data pipeline. The company's own reported results are the most striking of the three: a documented 48% increase in time on wing before first removal, directly tied to its AI-and-digital-twin-driven predictive maintenance program — a figure that, if broadly representative across its fleet, represents a substantially larger efficiency gain than either GE's or Pratt & Whitney's published figures.

2.4 Pratt & Whitney: The Scale-and-Diagnostics-First Approach

Pratt & Whitney's EngineWise platform, and specifically its ADEM (Advanced Diagnostics and Engine Monitoring) system, takes a somewhat more conservative, diagnostics-centric approach relative to Rolls-Royce's full digital-twin architecture or GE's platform-partnership model. ADEM provides machine-learning-based analytics across a very large monitored fleet — reported figures place this at over 10,000 to 11,000 in-service engines across roughly 140 customers, delivered to customers through the EngineWise Connect portal. Pratt & Whitney has publicly cited a 20% reduction in unscheduled engine removals attributable to this combination of physics-based models and data-driven analytics, though this specific figure traces to a 2022 company performance review and may understate more recent progress — a caveat worth flagging explicitly, since it means the comparison in Section 3 below is not perfectly apples-to-apples across identical reporting years. Pratt & Whitney has also been investing in "Connected Factory" pilots aimed at manufacturing-side efficiency (targeting up to 30% improvement in order fulfillment time and machine idle time) and has funded academic research — including a 2025-announced research chair at the University of Waterloo — specifically targeting machine-learning methods for gas turbine simulation, suggesting a longer-horizon research investment alongside its nearer-term ADEM deployment.

3. Three-Way Comparison Table

| Dimension | GE Aerospace | Rolls-Royce | Pratt & Whitney |

|---|---|---|---|

| Platform name | Palantir AIP/Foundry-powered architecture ("TrueChoice Defense" for military) | IntelligentEngine / Blue Data Thread | EngineWise / ADEM (Advanced Diagnostics and Engine Monitoring) |

| Core architecture philosophy | External AI platform partnership layered across commercial and defense data | Continuous automated data pipeline feeding physics-based digital twins, built with IFS | Diagnostics-and-analytics platform monitoring a very large fleet at scale |

| Key technology partners | Palantir Technologies | IFS (Maintenix), Microsoft Azure IoT, Siemens | Internal ADEM system; EngineWise Connect customer portal |

| Program origin | Expanding rapidly since 2025–2026 (though GE's broader digital efforts predate this) | 2018–2019 (among the earliest branded digital-twin programs in the sector) | Long-running; ADEM has monitored engines for over a decade, with continued upgrades |

| Reported headline efficiency figure | ~60% earlier fault detection; ~33% fewer unscheduled removals | 48% increase in time on wing before first removal | 20% reduction in unscheduled engine removals (2022-dated figure) |

| Monitored fleet scale (approximate) | 44,000+ commercial engines in service | [VERIFY: specific monitored-fleet figure for IntelligentEngine specifically] | 10,000–11,000+ engines, ~140 customers |

| Dual commercial/defense use | Explicit — same architecture serves CES and DPT segments | Primarily commercial-focused in public materials reviewed | Primarily commercial-focused in public materials reviewed, though Pratt & Whitney also serves military engine programs separately |

| Backlog/scale context | ~$190B total backlog, ~$170B commercial services (FY2025/Q1 2026) | [VERIFY: current Rolls-Royce services backlog figure] | [VERIFY: current Pratt & Whitney/RTX aftermarket backlog figure] |

Note: the headline efficiency figures in this table are not measured on identical timeframes, fleets, or methodologies — GE's figures are the most recent (2025–2026), Rolls-Royce's 48% figure derives from a case-study source without a precise publication date specified in the material reviewed, and Pratt & Whitney's 20% figure is explicitly dated to 2022. This is a genuine limitation of any cross-company comparison in this space, since none of the three companies publishes results using a shared, independently audited benchmark — a point worth keeping in mind before treating any single number as a definitive ranking.

4. What This Reveals About the Broader Race

A few patterns emerge once these three strategies are placed side by side, beyond the headline efficiency figures.

No two companies are building the same kind of thing, despite using similar language. "Digital twin," "predictive maintenance," and "AI-driven diagnostics" are used by all three companies, but they describe meaningfully different technical architectures — GE's is fundamentally a data-orchestration and AI-platform story, Rolls-Royce's is fundamentally a continuous physics-based simulation story, and Pratt & Whitney's is fundamentally a large-scale diagnostics-and-monitoring story. This matters for anyone evaluating vendor claims in this space generally: "we have a digital twin" or "we use AI for predictive maintenance" is a category description, not a specific, comparable capability claim.

Rolls-Royce's first-mover position hasn't obviously translated into a durable lead. Despite starting its branded digital-twin program years before GE's current Palantir push, Rolls-Royce doesn't appear to occupy a position of unambiguous technical dominance in the public reporting reviewed for this piece — all three companies are actively investing and publishing comparable-order-of-magnitude efficiency claims. This is broadly consistent with the assessment in our companion GE piece that this capability is trending toward table stakes across the industry rather than a durable, defensible edge for any single player.

The efficiency figures, taken together, tell a consistent qualitative story even if they're not directly comparable. A 20–60% improvement range across unscheduled removals or earlier fault detection, reported independently by all three major engine makers using different architectures, is a strong qualitative signal that AI-driven predictive maintenance is delivering real operational value across the industry — even though the lack of a shared, independently audited benchmark makes it impossible to say with confidence which company's approach is quantitatively "winning."

Vendor and partner dependency is a real, differentiating risk factor. GE's architecture is the most visibly dependent on a single external AI platform partner (Palantir); Rolls-Royce's depends significantly on its IFS partnership plus cloud/IoT infrastructure from Microsoft and Siemens; Pratt & Whitney's ADEM system appears the most internally built and controlled of the three based on available public materials. This has real implications for resilience and negotiating leverage that go beyond the headline efficiency numbers, and is worth factoring into any procurement or competitive analysis that treats these three programs as interchangeable.

5. What to Watch Next

- Whether any of the three companies publishes results using a shared, third-party-validated benchmark methodology, which would finally make the efficiency comparisons in Section 3 genuinely apples-to-apples rather than three independently reported, differently-dated figures.

- Pratt & Whitney's next EngineWise/ADEM performance update, given its most-cited public figure (20% fewer unscheduled removals) dates to 2022 — a refreshed figure would materially change how it stacks up against GE's and Rolls-Royce's more recent numbers.

- Whether Rolls-Royce announces a comparable large-scale AI platform partnership (echoing GE's Palantir relationship) to accelerate IntelligentEngine, or continues to rely primarily on its IFS-built Blue Data Thread architecture.

- Consolidation or new partnership announcements in this space generally, given how much of each company's current capability depends on a small number of external technology partners (Palantir for GE; IFS, Microsoft, and Siemens for Rolls-Royce).

- Whether military/defense-sector applications expand at Rolls-Royce or Pratt & Whitney the way GE has explicitly built out its dual-use commercial/defense architecture — this remains a clear point of differentiation worth tracking.

6. Anchor Data Point

Across three independently reported efficiency figures — GE's 33% reduction in unscheduled removals, Rolls-Royce's 48% increase in time on wing, and Pratt & Whitney's 20% reduction in unscheduled removals — no two engine makers measured their AI-driven predictive maintenance gains the same way, on the same timeframe, or against the same fleet, making the "digital twin race" a genuine competitive narrative without yet having a genuine, shared scoreboard.